Editorial Observe: We earn a fee from companion hyperlinks on Forbes Advisor. Commissions don’t have an effect on our editors’ opinions or evaluations.

The much-anticipated spring home-buying season by no means bloomed. In fact, it hardly even budded.

Now, housing market stakeholders need to summer time for a possible rebound, hoping that rising stock and slower residence worth appreciation will entice consumers off the sidelines by providing extra choices and better negotiating energy.

Nonetheless, the financial panorama stays unsure, with the specter of tariffs looming over shoppers. New residence builders are additionally dropping confidence, signaling a building slowdown forward amid excessive prices and weakened demand.

Moreover, elevated mortgage charges and residential costs have but to say no, leaving many aspiring residence consumers discouraged amid affordability challenges that specialists predict will seemingly persist all year long.

Housing Market Forecast 2025

U.S. residence costs posted a 2.7% annual achieve in April—the slowest annual appreciation since mid-2023—down from the three.4% progress launched in March, in keeping with the newest S&P CoreLogic Case-Shiller House Worth Index, which tracks single-family residence values and is calculated month-to-month utilizing a three-month transferring common.

This report displays residence gross sales from February by April. The interval was marked by increasing stock and a U-shaped motion within the common 30-year mortgage fee, which began on the higher 6% in February, dipped to the mid-6% vary in March and climbed again up in April to just about the place it started.

Regardless of slowing worth progress, the index nonetheless managed to succeed in one other document excessive.

But, at the same time as residence affordability stays a problem—and sure will for the foreseeable future—budget-conscious consumers nonetheless have choices in the event that they know the place to look.

“We’re witnessing a housing market in transition,” mentioned Nicholas Godec, head of fastened revenue tradables & commodities at S&P Dow Jones Indices, within the report. “The period of broad-based, speedy worth appreciation seems over, changed by a extra selective surroundings the place native fundamentals matter greater than nationwide traits.”

These in search of higher affordability can discover houses below $300,000 in Midwest metro areas reminiscent of Detroit, Cleveland and Dayton, Ohio, in keeping with a latest Redfin report rating the ten most cost-effective locations to purchase a house out of the 91 most populous U.S. metro areas. The metros of Buffalo, New York, St. Louis and Baton Rouge, Louisiana, with median costs below $300,000, additionally made the highest 10.

Will the Housing Market Crash in 2025?

With record-high residence costs nonetheless trending upward in lots of markets amid financial uncertainty, chances are you’ll be involved that we’re in a bubble that’s primed to pop, because it did within the 2008 monetary disaster. Nevertheless, the probability of a housing market crash (a speedy drop in unsustainably excessive residence costs on account of waning demand) stays low in 2025.

Housing inventory provide has risen considerably in comparison with final 12 months, but total stock continues to be effectively under pre-pandemic ranges.

“[T]he document low provide of homes available on the market protects in opposition to a market crash,” says Tom Hutchens, govt vp of manufacturing at Angel Oak Mortgage Options, a nonqualified mortgage lender.

Consultants are additionally fast to level out that right this moment’s owners are on way more safe footing than these popping out of the 2008 monetary disaster, with many having substantial residence fairness. What’s extra, a document variety of owners right this moment are mortgage-free.

When Will the Housing Market Get well?

At a minimal, for a housing restoration to happen, two main circumstances should enhance.

Housing Stock Wants To Enhance

“For the absolute best consequence, we’d first must see inventories of houses on the market flip significantly greater,” Keith Gumbinger, vp at on-line mortgage firm HSH.com, tells Forbes Advisor. “This extra stock, in flip, would ease the upward strain on residence costs, leveling them off or maybe serving to them to settle again considerably from peak or near-peak ranges.”

Mortgage Charges Want To Fall

Moreover, mortgage rates want to say no to see a significant enhance in housing market exercise.

Nevertheless, with charges firmly caught above 6.5% for over seven months, hopes are dwindling for a lot enchancment over the rest of the 12 months. If the Federal Reserve cuts its key rate of interest additional, this might not directly trigger mortgage charges to fall—not less than to some extent.

Nevertheless, with a lot financial uncertainty and volatility, what the Fed does subsequent is troublesome to foretell.

Even so, Gumbinger warns that charges cooling too shortly might create a surge in demand that may wipe away any stock features, inflicting residence costs to surge. He provides that mortgage charges ultimately returning to a extra “regular” upper-4%-to-lower-5% vary can be useful to the housing market however predicts it could possibly be some time earlier than we return to these charges.

How Do Right now’s Month-to-month Funds and Lengthy-Time period Curiosity Prices Evaluate to Final Yr?

The Forbes Advisor mortgage calculator makes it simple for brand spanking new owners to estimate what they’ll pay month-to-month and the way a lot curiosity they’ll shell out in the long term.

For example, a typical residence in Could 2025 price roughly $368,000 in keeping with Zillow knowledge. Patrons who put down 20% on a typical residence and financed at a 6.89% mortgage fee—the common 30-year fixed mortgage rate the final week of Could—have a month-to-month principal and curiosity cost of $1,936.

In distinction, owners who purchased a typical residence on the similar time in 2024, when the everyday worth was round $365,000 and the mortgage fee was 7.03%, are paying $1,948 a month.

On this situation, new owners are paying $12 much less every month and saving $6,583 in mortgage curiosity over the lifetime of the mortgage in comparison with consumers who bought houses a 12 months in the past. Whereas not a major distinction, you may get a way how the speed decline many are holding out for might considerably cut back month-to-month funds and bolster total curiosity financial savings.

Keep in mind, although, you’ll additionally must pay month-to-month property taxes and insurance coverage and probably different prices reminiscent of owners affiliation charges or extra owners insurance coverage protection. Coming into these particulars into our calculator offers you a extra correct view of your month-to-month prices.

Professional Tip

Use the Forbes Advisor mortgage calculator to see how totally different charges can influence your month-to-month funds.

Residential Actual Property Stats: Current, New and Pending House Gross sales

The spring home-buying season died on the vine. Nevertheless, there are some indicators that gross sales exercise might warmth up this summer time.

Right here’s a take a look at what’s occurring within the housing market.

Current-House Gross sales

Current-home gross sales, which embrace accomplished transactions of single-family houses, townhomes, condominiums and co-ops, struggled to eke out a optimistic studying amid steep mortgage charges, record-high residence costs and financial jitters.

The Nationwide Affiliation of Realtors (NAR) reported that month-to-month gross sales rose simply 0.8% in Could, placing the seasonally adjusted annual gross sales fee at 4.03 million, up barely from 4 million in April. Yr-over-year gross sales slid 0.7%.

Whereas gross sales remained anemic, stock maintained its upward trajectory, reaching its highest stage in 5 years.

Resale housing inventory jumped 9% from the earlier month and 20.3% from a 12 months in the past. Current unsold stock stands at a 4.6-month provide on the present month-to-month gross sales tempo, up from 4.4 months in April. Most specialists think about a balanced market to be between 4 and 6 months.

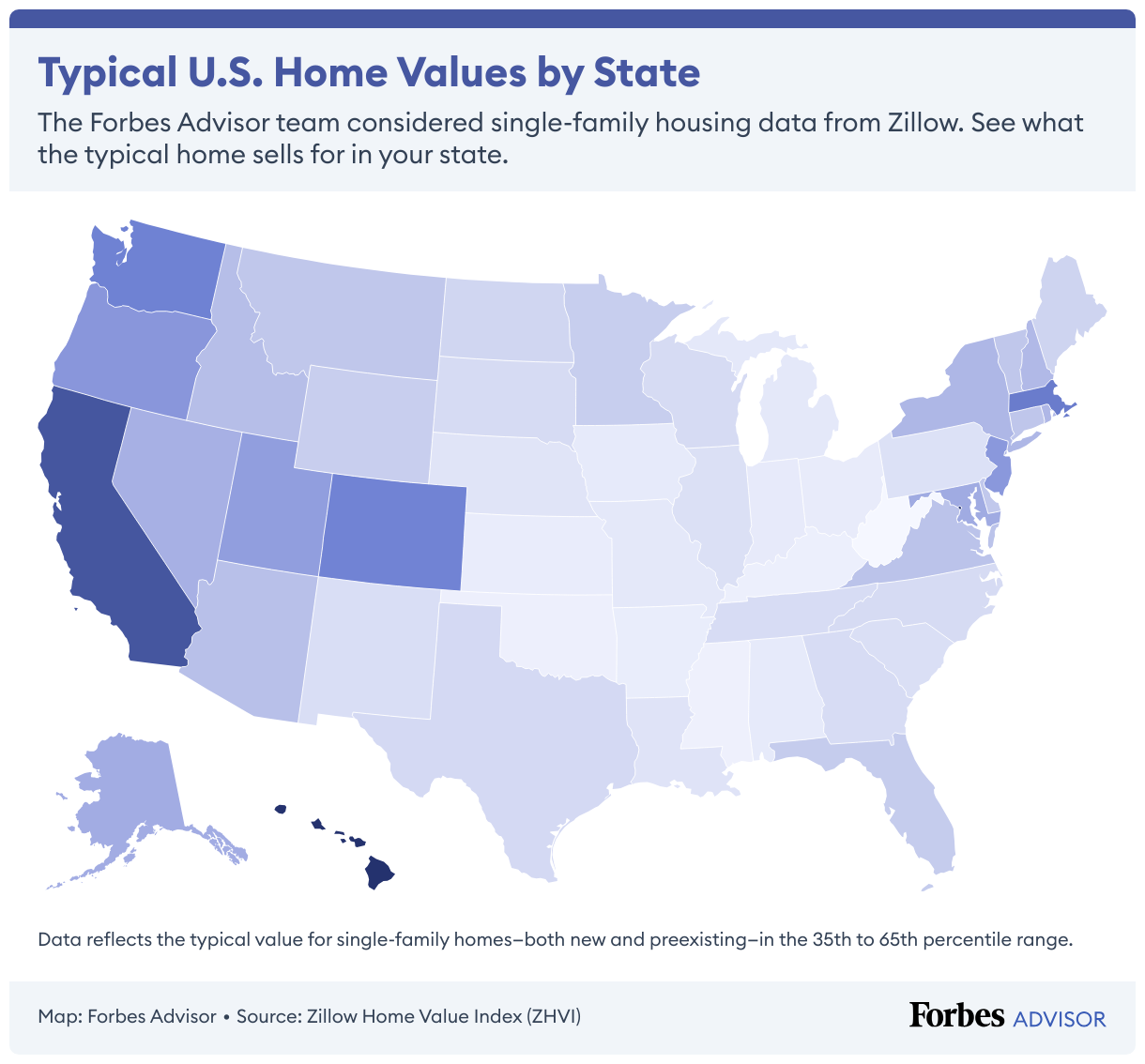

In the meantime, residence worth progress continues, although the tempo is decelerating. The nationwide median resale residence worth rose 1.3% from a 12 months in the past to $422,800, marking the very best Could on document and the twenty third straight month of year-over-year worth progress.

Nevertheless, regional worth disparities stay pronounced. For instance, the median resale residence worth within the Midwest rose 3.4% from a 12 months in the past to $326,400, in comparison with the West, which rose 0.5% to $633,500.

New House Gross sales

Gross sales of newly constructed houses took a notable dip in Could.

The newest U.S. Census Bureau and U.S. Division of Housing and City Improvement (HUD) knowledge revealed that seasonally adjusted new residence gross sales decreased 13.7% between April and Could, and 6.3% in comparison with final 12 months.

Solely the Northeast noticed a month-to-month and annualized gross sales enhance, whereas the Midwest, South and West recorded decreases.

Month-to-month stock rose from 8.3 months to 9.8 months provide, which additionally surpasses the 8.5-month stage recorded a 12 months in the past.

“Taken collectively, will increase in stock and month’s provide, mirror the pattern of softening demand within the current residence sale market,” mentioned Jake Krimmel, senior economist at Realtor.com, in an emailed assertion. “Whether or not the brand new and current residence sale markets proceed to maneuver in tandem will probably be one thing to look at going ahead this summer time.”

But, at the same time as gross sales slumped, costs edged greater. The median new residence gross sales worth rose by 3.7% in Could to $426,600 and three% from a 12 months in the past, in keeping with the info.

Latest House Gross sales Information

Supply: U.S. Census Bureau, HUD and NAR

*Rounded to the closest p.c

Pending House Gross sales

Whereas new and existing-home gross sales had been subdued, an increase in contract signings supplied some optimism.

NAR’s Pending Properties Gross sales Index rose 1.8% between April and Could, with all 4 U.S. areas posting month-to-month will increase. In comparison with final 12 months, pending transactions had been up 1.1%, with the Midwest and South posting features, whereas the Northeast and West recorded declines.

A pending residence sale marks the purpose within the buy transaction when the customer and vendor agree on worth and phrases and is taken into account a number one indicator of a closed current residence sale inside the subsequent one to 2 months.

So, how promising is that this studying? May it’s {that a} housing market turnaround is lastly across the nook?

“On one hand, Could’s pending residence sale enhance could possibly be an indication of consumers lastly starting to get off the sidelines because the market balances,” Krimmel mentioned. “On the opposite, rates of interest have been steadily rising all through the spring home-buying season, and with the Federal Reserve holding regular, this might proceed into the summer time months.”

Housing Stock Forecast: When Will There Be Ample Provide To Cut back Costs?

After a number of years of record-low stock, the provision of houses has risen notably over the previous 12 months. If the pattern continues, consumers sidelined by affordability challenges could discover themselves with extra choices—so long as they know the place to look

Listed here are elements impacting the stock panorama.

The Lock-In Impact is Starting To Unlock

Rick Sharga, founder and CEO of CJ Patrick Firm, a market intelligence and enterprise advisory agency, tells Forbes Advisor that stock is up over 33% from 2024 and seems to be on monitor to hit pre-pandemic ranges by the tip of the 12 months, or probably earlier.

There are a number of causes for this enchancment, one in all which is the loosening of the “lock-in impact,” a state of affairs the place owners with ultra-low charges—such because the high-2% to 4% charges seen throughout the pandemic years—are disincentivised to promote on account of their charges being effectively under present ranges.

“Price lock continues to be a professional concern, however changing into much less of a problem over time,” says Sharga.

Certainly, in keeping with actual property tech firm Redfin, 82.8% of householders right this moment have charges under 6% down from a excessive of 92.7% in mid-2022.

Nevertheless, there are nonetheless many owners sitting on an excellent fee who want a serious life occasion motive to promote, reminiscent of a job switch, job loss, marriage, divorce or demise, says Sharga.

What’s Driving the Stock Progress? It Will depend on the Area

The general market nonetheless barely favors sellers, as provide stays close to the decrease finish of what’s thought-about a balanced market.

Nevertheless, stock ranges range extensively by area. Markets like Austin and San Antonio, Texas, and Tampa, Florida, the place costs surged throughout the pandemic, are seeing elevated provide and slowing worth progress.

“[T]listed below are quite a few states, notably Florida and Texas, which have already got extra on the market stock than they did previous to the pandemic, and the place demand has weakened,” says Sharga. “In these areas, the market is tilting in favor of consumers.”

On the flip aspect, areas within the Midwest and components of the Northeast—reminiscent of Buffalo and Rochester, New York, Cleveland and Pittsburgh—that didn’t expertise skyrocketing worth will increase and a surge in newly-built houses have decrease stock and face elevated competitors amongst consumers.

How Declining Mortgage Charges May Affect Provide, House Costs

Given the pent-up demand for houses, a decline in mortgage charges—particularly a pointy one—might shortly shrink housing provide.

“We’re in an extremely rate-sensitive surroundings right this moment, and each time we’ve seen mortgage charges drop into the low-to-mid 6% vary, we’ve seen an inflow of consumers hit the market,” says Sharga.

Sharga provides that charges dropping to six% would seemingly encourage extra owners to promote. Even so, he says many consumers will nonetheless be shut out of the market on account of different rising home-related prices.

“[H]ome costs have gone up virtually 50% over the previous 5 years, property taxes have risen together with them, and house owner’s insurance coverage premiums rose by 24% between 2020-2024,” says Sharga. “So though there’s positively some pent-up demand, a one-point dip in mortgage charges in all probability wouldn’t carry so many consumers to market that it will overwhelm the provision and trigger one other big spike in residence costs.”

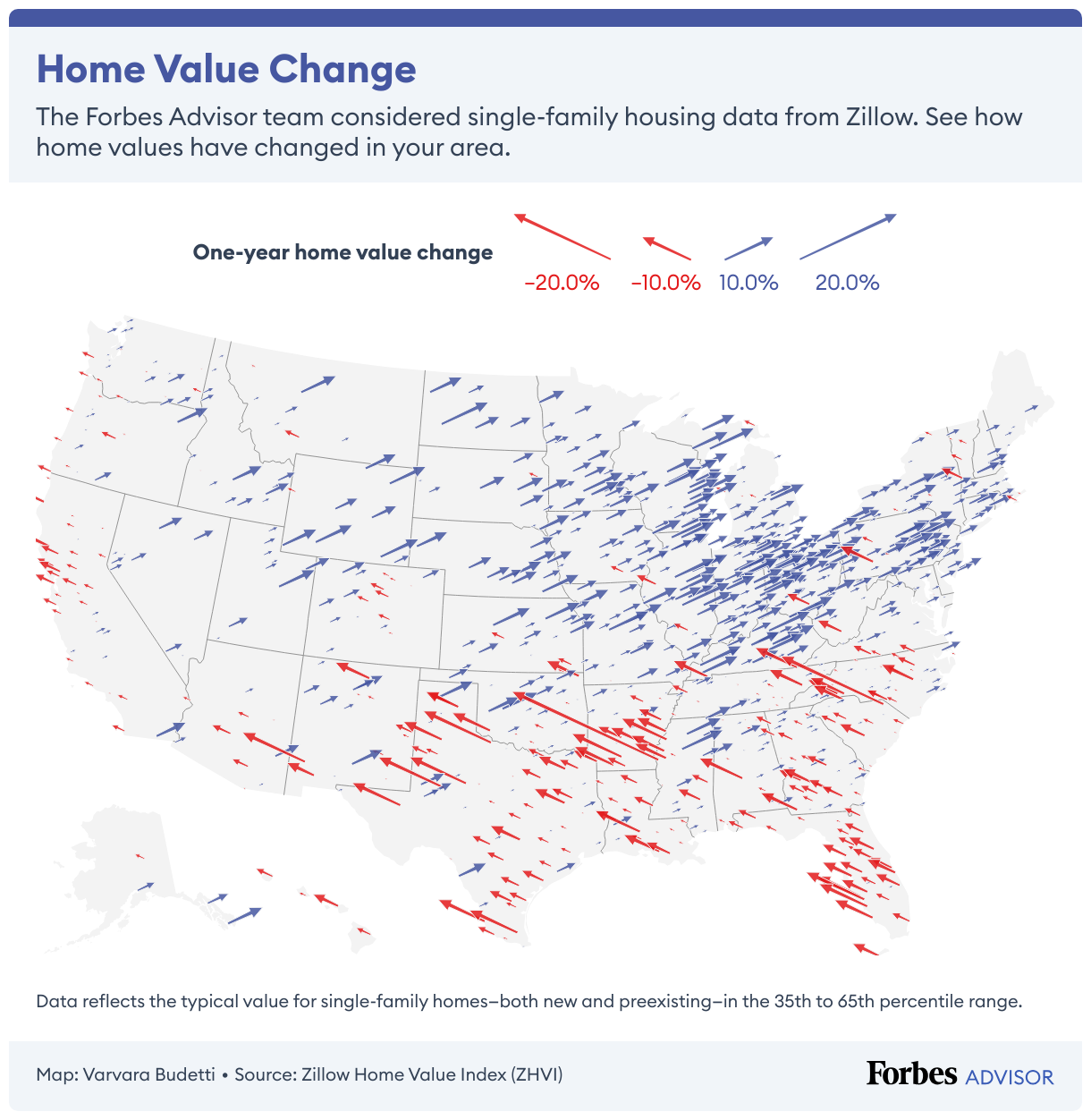

And talking of residence costs, right here’s what the newest residence values appear to be across the nation.

Commerce Insurance policies and Financial Uncertainty Drag Down Builder Sentiment, New House Development

Builder sentiment declined once more and new single-family housing begins slipped, as financial volatility and elevated mortgage charges proceed to discourage consumers and strain builders.

Builder Confidence Sinks As Resale Stock Grows and Patrons Pull Again

Builder sentiment continues to erode. The Nationwide Affiliation of House Builders (NAHB)/Wells Fargo Housing Market index dropped from 34 to 32 in June—the third lowest studying since 2012—due to commerce coverage headwinds, elevated mortgage charges and financial jitters. A studying of fifty or above means extra builders see good circumstances forward for brand spanking new building.

The final time a studying was above 50 was April 2024.

May This Summer season Be the Greatest Time To Snag a Scorching Deal on a New House?

Nevertheless, unhealthy information for builders is popping out to be excellent news for consumers hoping to buy a newly-built residence.

“To assist tackle affordability issues and convey hesitant consumers off the fence, a rising variety of builders are transferring to chop costs,” Hughes mentioned.

Certainly, the portion of builders providing worth cuts in June rose from 34% in Could to 37%, the very best determine since 2022, when NAHB started monitoring this knowledge month-to-month.

Builders have additionally been feeling the squeeze from the rising provide of resale houses, which has pushed down existing-home costs, and added strain on new residence costs and gross sales.

New House Begins Decline Amid Financial system Worries, Tariffs and Purchaser Pullback

Potential residence consumers, take heed: A slowdown in new building exercise seems to be underway.

Single-family housing begins edged up 0.4% in Could from the earlier month however dropped 7.3% from a 12 months in the past, in keeping with the newest U.S. Census Bureau and HUD knowledge. Completions jumped 8.1% from April to Could, however had been primarily flat in comparison with a 12 months in the past.

The decline in annualized housing begins coupled with sinking builder sentiment suggests consumers could face a smaller choice—and elevated competitors—this time subsequent 12 months.

What’s Forward for Foreclosures within the Second Half of 2025?

Lenders started foreclosures on 24,165 properties nationwide in Could, down 4% from the earlier month however up 8% from final 12 months, in keeping with actual property knowledge agency Attom.

Whereas knowledge on foreclosures begins was combined, accomplished foreclosures knowledge revealed month-to-month and yearly features, with real estate-owned properties, or REOs, rising 7% in comparison with April and surging 34% year-over-year. REOs are houses that didn’t promote at foreclosures auctions, with mortgage lenders in the end taking possession.

Foreclosures Spike Places Consultants on Alert

The spike in REOs in latest months is beginning to elevate eyebrows.

Nonetheless, analysts stay unsure whether or not that is an precise purple flag or factors extra to a short lived systemic subject.

“[L]enders should be working by a backlog of current instances,” mentioned Rob Barber, CEO at Attom, within the report. “We’ll be watching intently within the months forward to see how these traits evolve.”

Though the rise in REOs is prompting some concern, foreclosures exercise nonetheless stays traditionally low.

For context, Attom knowledge exhibits 2024 foreclosures exercise at 35% under 2019 ranges, earlier than the Covid-19 pandemic emerged and upended the housing market. 2024 foreclosures filings had been down near 90% in comparison with 2010, after they peaked at almost 2.9 million.

Regardless of latest spikes in exercise, residence fairness positions stay robust, serving as a buffer in opposition to a pronounced escalation of delinquencies.

Close to-File House Fairness Helps Curb Foreclosures

Sharga explains {that a} vital issue contributing to right this moment’s comparatively low ranges of foreclosures exercise is that owners—together with these in foreclosures—possess an unprecedented quantity of home equity.

Certainly, house owner fairness grew by almost $600 billion between the primary quarters of 2024 and 2025, in keeping with knowledge from the Federal Reserve Financial institution of St. Louis. Though down from the record-high of $35.6 trillion in second quarter of 2024, whole house owner fairness stands at over $34.7 trillion—the fourth-highest worth on document.

Elevated residence fairness ranges proceed to perpetuate a excessive share of equity-rich mortgages (when an impressive mortgage stability is at or under 50% of a house’s estimated market worth). Over 46% of mortgaged houses had been equity-rich throughout the first quarter of 2025, in keeping with Attom’s newest U.S. House Fairness and Underwater Report.

Though this share is under the 49.2% peak recorded within the second quarter of 2024 and 47.7% within the final quarter of 2024, the determine continues to be almost double the 26.5% stage posted within the first quarter of 2020, per Attom knowledge.

“For a house owner within the early stage of foreclosures, that fairness helps them keep away from a foreclosures sale, both by leveraging the fairness to pay down late mortgage payments, or by promoting their property to be able to shield the fairness they’d in any other case lose on the public sale,” Sharga says.

Will 2025 Be a Good Yr To Purchase a House?

Buying a house—in any market—is a extremely private determination. As a result of houses symbolize the biggest single buy most individuals will make of their lifetime, it’s essential to be in a strong monetary place earlier than diving in.

Use a mortgage calculator to estimate your month-to-month housing prices primarily based in your down cost. However in the event you’re attempting to foretell what may occur in 2025, specialists say that is in all probability not one of the best home-buying strategy.

“The housing market—like so many different markets—is sort of unimaginable to time,“ Orphe Divounguy, senior macroeconomist at Zillow House Loans, says. “The most effective time for potential consumers is after they discover a residence that they like, that meets their household’s present and foreseeable wants and that they will afford.”

Gumbinger agrees it’s exhausting to inform would-be owners to attend for higher circumstances.

“Extra usually, it appears the case that residence costs typically hold rising, so the goalposts for amassing a down cost hold transferring, and there’s no assure that tomorrow’s circumstances will probably be all that a lot better within the combination than right this moment’s.”

Divounguy says “getting on the housing ladder” is worth it to start constructing fairness and web value.

Professional Ideas for Patrons and Sellers

Listed here are some knowledgeable tricks to enhance your probabilities for an optimum consequence on this tight housing market.

Professional Ideas for Shopping for in Right now’s Actual Property Market

Hannah Jones, a senior financial analysis analyst at Realtor.com, provides this knowledgeable recommendation to aspiring consumers:

- Know your finances. As an alternative of specializing in worth, figure out how much you can afford as a month-to-month cost. Your month-to-month housing cost is influenced by the value of the house, your down cost, mortgage fee, mortgage time period, residence insurance coverage and property taxes.

- Be versatile about residence dimension and site. Maybe your finances is enough for a small residence in your excellent neighborhood or a bigger, newer residence additional out. Understanding your priorities and having some flexibility might help you progress shortly when an acceptable residence enters the market.

- Control the market the place you hope to purchase. Decide the world’s obtainable stock and worth ranges. Additionally, take note of how shortly houses promote. Not solely will you be tuned in when one thing nice hits the market, you possibly can really feel extra assured transferring ahead with buying a well-priced residence. A real estate agent might help with this.

- Don’t be discouraged. Buying a house is among the largest monetary choices you’ll ever make. Approaching the market confidently, armed with good info and grounded expectations will take you far. Don’t let the hustle of the market persuade you to purchase one thing that’s not in your finances, or not proper to your way of life.

…All the time get pre-approved with a robust and respected lender as quickly as attainable. Getting pre-approved offers you a a lot clearer understanding of your finances and what you possibly can afford, it exhibits sellers that you simply’re a professional purchaser and it strengthens your provides.

— Scott Bridges, senior managing director at Pennymac and Forbes Advisor advisory board member

Professional Ideas for Promoting in Right now’s Actual Property Market

Gary Ashton, founding father of The Ashton Actual Property Group of RE/MAX Benefit, has this knowledgeable recommendation for sellers:

- Analysis comparable residence costs in your space. Sellers must have probably the most up-to-date pricing intel on comparable homes promoting of their market. Know the market competitors and worth the house competitively. As well as, perceive that in some worth factors it’s a purchaser’s market—you’ll must be ready to make some concessions.

- Make sure that your property is in top-notch form. Properties must be in nice situation to compete and create a robust “on-line curb attraction.” Effectively-maintained houses and enticing entrance yards are main options that consumers search for.

- Work with a neighborhood actual property agent. An actual property agent or group with a robust native advertising and marketing presence and entry to main actual property portals can provide vital worth and allow you to land an excellent deal.

- Don’t delay points that require consideration. Put together the house by making any repairs or enhancements. Eradicating any objections that consumers may even see helps focus the customer on the optimistic attributes of the house.

Discover the Greatest Mortgage Lenders of 2025

Ceaselessly Requested Questions (FAQs)

Will declining mortgage charges trigger residence costs to rise?

Declining mortgage charges will seemingly incentivize would-be consumers anxious to personal a house to leap into the market. Anticipate this elevated demand amid right this moment’s tight housing provide to place upward strain on residence costs.

What is going to occur if the housing market crashes?

Most specialists don’t anticipate a housing market crash in 2025 since many owners have constructed up vital residence fairness. The problem is primarily an affordability disaster. Excessive rates of interest and inflated residence values have made buying a house difficult for first-time residence consumers.

Is it sensible to purchase actual property earlier than a recession?

If you happen to’re in a monetary place to purchase a house you intend to stay in for the long run, it gained’t matter while you purchase it as a result of you’ll stay in it by financial highs and lows. Nevertheless, if you’re trying to purchase actual property as a short-term funding, it is going to include extra threat in the event you purchase on the top earlier than a recession.