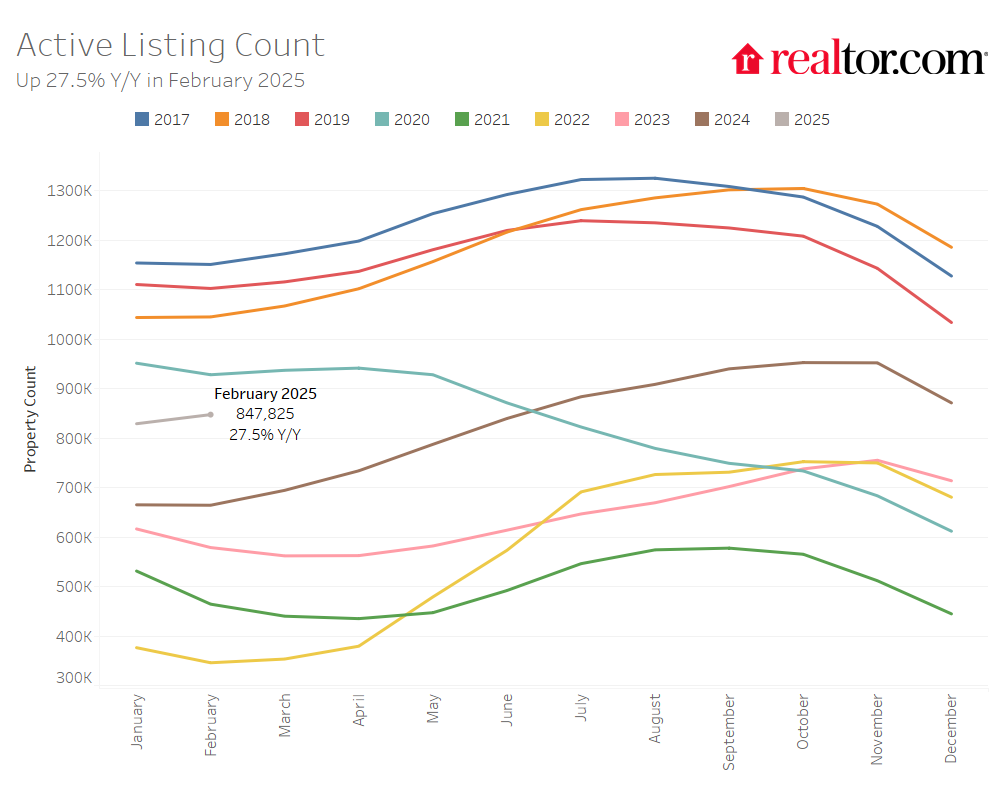

- The variety of houses actively on the market continues to be greater in comparison with final yr, rising by 27.5%, a sixteenth straight month of development.

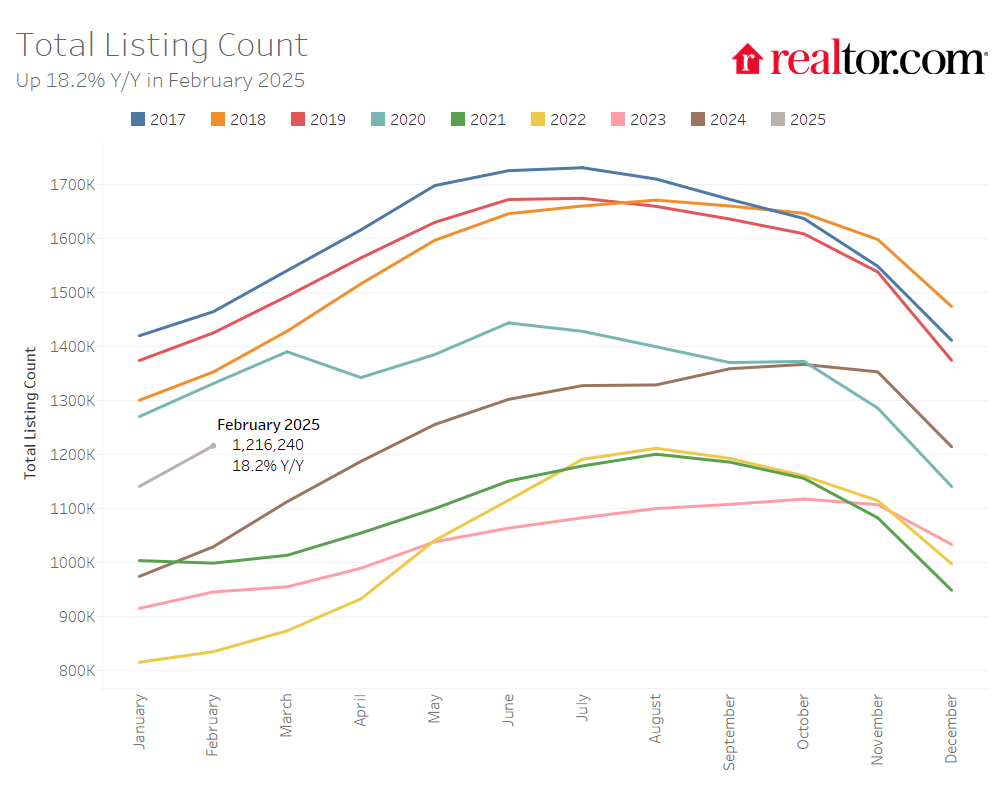

- The full variety of unsold houses, together with houses which might be below contract, elevated by 18.2% in contrast with final yr.

- Sellers listed their houses at larger charges than final yr, with newly listed houses growing 4.2% year-over-year, a bit decrease than January’s tempo.

- The median value of houses on the market this February was down 0.8 % in contrast with final yr, at $412,000. Nevertheless, extra small houses are being listed this yr, which decreased the median listing value relative to final yr. The median listing value per sq. foot, which controls for dimension, grew by 1.2%, indicating that residence values proceed to extend.

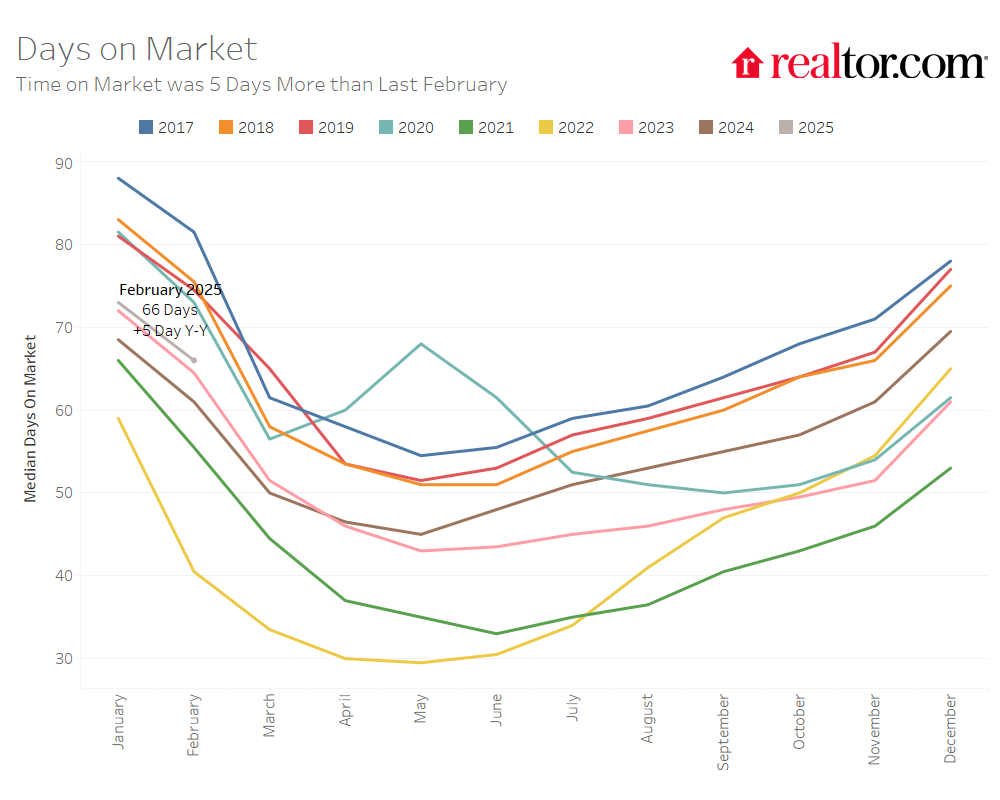

- Houses spent 66 days available on the market. That is 5 days greater than final yr.

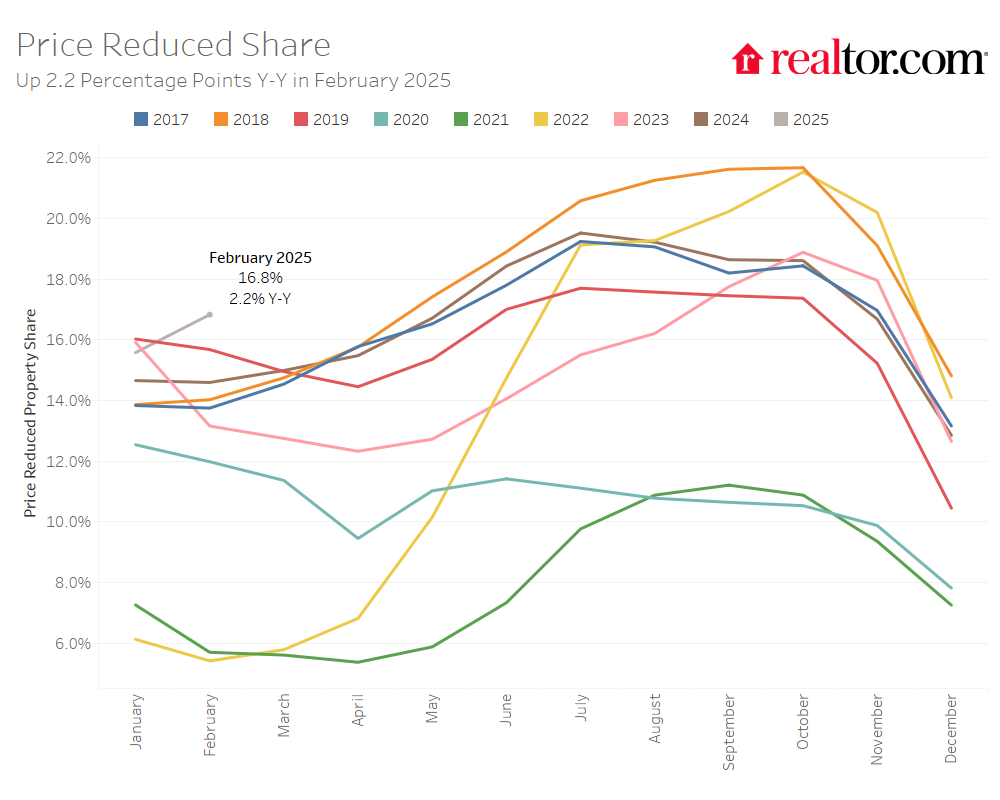

- The share of listings with value cuts grew as soon as once more in contrast with final yr, with 16.8% of sellers slicing costs within the month of February, up from 14.6% in February 2024.

In line with the Realtor.com® February housing data, sellers are more and more adjusting to slower market situations, because the share of houses with value reductions rose considerably final month. This pattern may point out a possible slowdown in value development. In February, the nation’s median residence itemizing value dipped under final yr’s degree. Nevertheless, when accounting for the next proportion of smaller houses available on the market, the worth per sq. foot nonetheless confirmed year-over-year development. Even so, the rise in value reductions suggests the market could proceed to melt. On a constructive notice, whereas rates of interest stay elevated, decrease costs may encourage extra patrons to enter the market this spring.

In the meantime, housing markets with a major variety of federal staff are drawing consideration because the Trump Administration’s cost-reduction insurance policies take impact. Thus far, there isn’t any clear connection between the markets experiencing essentially the most important slowdowns and people with a big authorities workforce. Nevertheless, native housing developments are sometimes influenced by employment situations, so these areas might even see modifications over time. Whereas some results are anticipated, the complete image continues to be creating.

New Listings and General Stock Proceed to Improve

There have been 27.5% extra houses actively on the market on a typical day in February in contrast with the identical time in 2024, marking the sixteenth consecutive month of annual stock development. This is a rise from January, which was up solely 24.6% year-over-year. Nevertheless, whereas stock this February continues to enhance, it’s nonetheless down 22.9% in contrast with typical 2017 to 2019 ranges.

The full variety of houses on the market, together with houses that have been below contract however not but offered, elevated by 18.2% in contrast with final yr, rising on an annual foundation for the fifteenth month in a row. That is up barely from 17.1% final month.

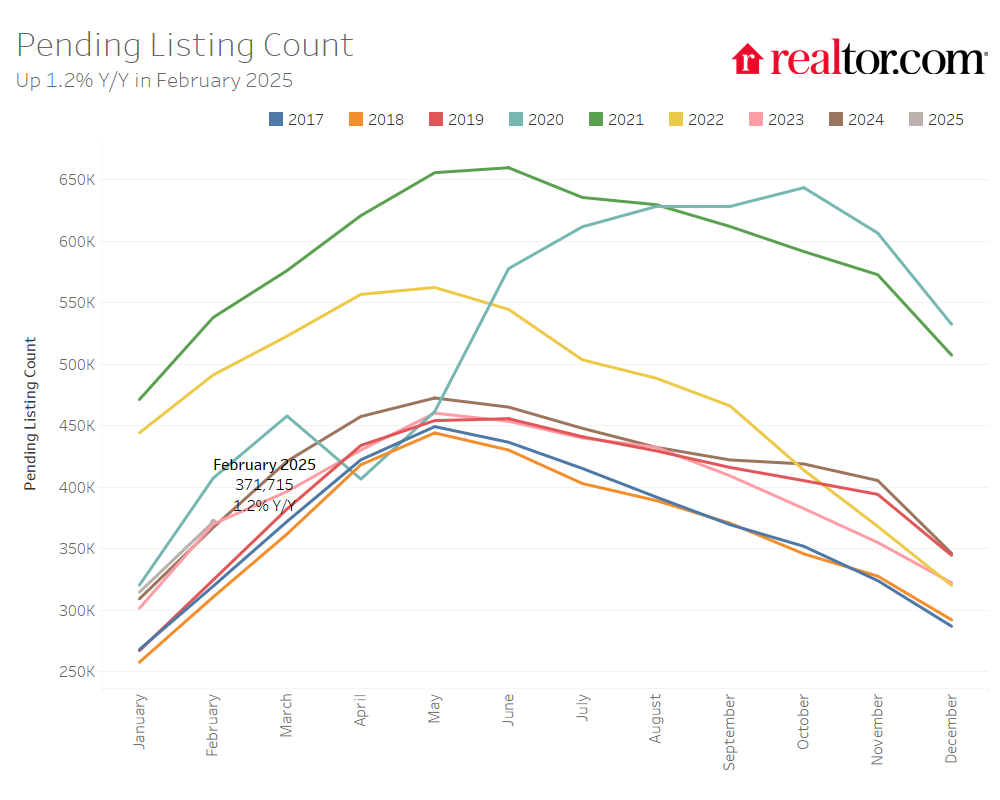

The variety of houses below contract however not but offered (pending listings) continued to rebound in February, growing by 1.2% in comparison with final yr. Nevertheless, it’s lower than January’s achieve of 1.8% and far lower than December’s 7.4% achieve. This slowdown is no less than partially as a consequence of mortgage charges being greater in January and February in comparison with the earlier months. Although charges are considerably greater right this moment than they have been only a few months in the past, our 2025 forecast exhibits that as each decrease charges and time chisel away on the “lock-in” impact that has held again gross sales this yr, we should always anticipate residence gross sales to rise modestly by 1.5% in 2025.

On the intense aspect, sellers elevated their exercise this February as newly listed houses have been 5.1% above final yr’s ranges, nevertheless this can be a lower from January’s rise of 10.8%. This places new itemizing exercise at its highest February degree since 2021. Whereas charges stay elevated, it’s doable that we could be seeing that chiseling impact beginning as sellers could develop uninterested in ready for important modifications in charges.

Regional and Metro Space Stock Developments

Fifteen Southern and Western Metros Have Extra Stock Than Pre-Pandemic Ranges

In February, all 4 areas continued to see lively stock develop over the earlier yr. The West noticed listings develop by 37.4%, whereas stock grew by 29.9% within the South, 18.7% within the Midwest, and 9.2% within the Northeast. In contrast with the standard February from 2017 to 2019 earlier than the COVID-19 Pandemic, the stock hole was smallest within the South and West, down by 7.0% and 9.1%, respectively. Stock was down by a bigger 45.0% within the Midwest and 58.4% within the Northeast.

The stock of houses on the market elevated in the entire largest metros in contrast with final yr. Metros that noticed essentially the most stock development included Denver (+64.4%), San Diego (+61.3%), and Las Vegas (+60.8%).

Regardless of greater stock development in contrast with final yr, most metros nonetheless had a decrease degree of stock in comparison with pre-pandemic years. Among the many 50 largest metro areas, 15 metros noticed greater ranges of stock in February in contrast with typical 2017 to 2019 ranges. This quantity is barely greater than final month’s listing of 14 metros. The highest metros that noticed stock surpass pre-pandemic ranges have been predominantly within the South and West and included Denver (+57.0%), San Antonio (+46.9%), and Dallas (+39.1%).

The West Noticed Newly Listed Houses Improve the Most In contrast With Final Yr

The West noticed the most important development in new listings, by 14.4% in contrast with final yr, whereas they grew by solely 3.7% within the South, and so they declined by 3.2 within the Midwest and three.4% within the Northeast The hole in newly listed houses in contrast with pre-pandemic 2017 to 2019 ranges was lowest within the South, the place newly listed houses have been simply 5.8% under pre-pandemic ranges. As compared, they have been down 15.7% within the West, 20.5% within the Midwest, and 34.6% within the Northeast.

In February, 35 of the 50 largest metros noticed new listings enhance over the earlier yr, down from 42 final month. Simply eight massive metros – together with San Antonio, Houston, and Jacksonville – noticed extra newly listed houses this February in contrast with the standard tempo of recent listings from February 2017 to 2019. That is up from six massive metros within the prior month. The metros that noticed the most important development in newly listed houses in contrast with final yr included San Jose (+28.0%), San Francisco (+27.2%), and Los Angeles (+27.1%).

Houses Are Staying on the Market Longer Than Final Yr however Shifting Sooner Than Pre-Pandemic

The standard residence spent 66 days available on the market this February, which is 5 extra days than the identical time final yr. This marks the eleventh month in a row the place houses spent extra time available on the market in contrast with the earlier yr. Nevertheless, the time a typical residence spends available on the market continues to be 11 days lower than the common February from 2017 to 2019.

Regional and Metro Space Time on the Market Developments

Within the Midwest, houses are spending eight extra days available on the market in comparison with final yr, whereas they’re up seven days within the South, 4 within the West, and a pair of within the Northeast.

Nevertheless, regardless of being up in comparison with final yr, in all 4 areas, time on market was at or nonetheless under pre-pandemic ranges. Within the West, houses spent the identical period of time available on the market in comparison with the 2017 to 2019 February common. Within the South, they spent eight days much less, and within the Midwest and Northeast houses are nonetheless shifting a lot quicker than pre-pandemic ranges, at 19 and 24 days much less, respectively.

In the meantime, time available on the market elevated in contrast with final yr in 42 of the 50 largest metro areas this February, down barely from 43 markets final month. It elevated essentially the most in Portland (+21 days), and Nashville, Atlanta and Jacksonville which tied at 16 extra days. Nineteen markets noticed houses spend extra time available on the market than typical 2017 to 2019 pre-pandemic timing, with a number of notable standouts: Portland (+31 days), Buffalo (+15 days), and Denver (+14 days).

Itemizing Value Reductions Level to Potential Value Softening

The nationwide median listing value in February was $412,000, which is 0.8% decrease than final February. Nevertheless, when a change within the mixture of stock towards smaller houses is accounted for, the standard residence listed this yr has elevated in asking value in contrast with final yr. The median itemizing value per sq. foot elevated by 1.2% in February in contrast with the identical time final yr. Furthermore, the standard listed residence value has grown by 39.2% in contrast with February 2019, whereas the worth per sq. foot grew by 54.8%.

The share of houses with value reductions throughout February was up 2.2 share factors from final yr, at 16.8%. What’s extra, the general share of stock with value cuts was greater than any February in our data since 2016 and is displaying extremely uncommon seasonal development. This excessive share of value reductions may sign additional value softening within the coming months as sellers alter their expectations to market situations.

Regional and Metro Space Value Developments

In contrast with final yr, the median listing value in February was down by 2.0% within the South, 1.2% within the West, 0.2% Midwest, and it was flat within the Northeast. Nevertheless, controlling for the combination of houses available on the market by price-per-square-foot, costs grew by 2.9% within the Northeast, 1.6% within the Midwest, and 0.9% within the West, however have been down 0.1% within the South the place stock development has been biggest. Amongst massive metros, the median listing value in Cleveland (+14.0%), Windfall (+7.0%), and Hartford (+6.6%) noticed the most important will increase.

In the meantime, all 50 massive metropolitan areas have seen value development in contrast with houses listed earlier than the pandemic. The markets the place sellers noticed the best enhance within the median listing value since February 2019 included Memphis (+59.4%), Boston (+52.8%), and Las Vegas (+51.2%). Markets which noticed the bottom return included San Francisco (+1.5%), Detroit, (+9.1%), and Minneapolis (+11.6%).

In contrast with final yr, the share of houses on the market with value reductions was up simply 0.2 share factors within the Northeast, however up 1.2 share factors within the Midwest, 2.1 share factors within the South, and three.5 share factors within the West. In comparison with typical pre-pandemic ranges, the share of value reductions is up within the South and West, by 3.5 and a pair of.2 share factors, respectively. The shares are nonetheless down 0.8 and a pair of.6 share factors within the Midwest and Northeast, respectively.

Forty-five of the 50 largest metros noticed the share of value reductions enhance in contrast with final February, up from 41 in January. Denver noticed the best enhance (+8.0 share factors), adopted by Charlotte (+6.4 share factors), and Tucson (+6.3 share factors).

Focus Shifts to Washington, D.C., and Different Federal Workforce Hubs

Because the Trump Administration rolls out cost-saving measures, some federal staff have chosen to depart their roles whereas others have seen their positions eradicated , with extra doubtlessly dealing with modifications sooner or later. The well being of an area housing market is commonly tied to the well being of the native labor market. Federal workforce reductions may have ripple results on housing markets with a excessive focus of presidency staff. Among the many 50 largest metro areas, Washington, D.C., and Virginia Seaside stand out for his or her excessive ratio of federal staff. Nevertheless, as of February, these markets haven’t proven notable developments in stock development, growing time on market, softening costs, or value reductions. For now, housing situations in these areas aren’t notably totally different from different markets. Our prior research means that the standard residence vendor takes no less than two weeks and infrequently longer to arrange a house on the market, so any actual affect is probably going forward.

Within the Washington, D.C., space, value reductions elevated by 2.3 share factors in comparison with final February, pretty in step with the nationwide pattern, putting it twenty third on the listing of metros with the most important will increase in value reductions—in regards to the center of the rating. The median listing value per sq. foot has additionally declined yr over yr, by 3.3%, with the metro rating twenty first when it comes to value declines. Notably, Washington, D.C.’s share of value reductions has risen every week all through February, suggesting that broader results may turn into extra obvious because the spring market unfolds. Consumers and sellers within the area could need to monitor developments carefully because the market continues to regulate.

February 2025 Regional Statistics

| Area | Lively Itemizing Depend YoY | New Itemizing Depend YoY | Median Itemizing Value YoY | Median Itemizing Value Per SF YoY | Median Days on Market Y-Y (Days) | Value-Lowered Share Y-Y (Proportion Factors) |

| Midwest | 18.7% | -3.2% | -0.2% | 1.6% | 8 | +1.2 pp |

| Northeast | 9.2% | -3.4% | 0.0% | 2.9% | 2 | +0.2 pp |

| South | 29.9% | 3.7% | -2.0% | -0.1% | 7 | +2.1 pp |

| West | 37.4% | 14.4% | -1.2% | 0.9% | 4 | +3.5 pp |

February 2025 Housing Overview of the 50 Largest Metros

| Metro Space | Federal Authorities Worker Share of Whole Employment (Dec 2024) | Median Itemizing Value | Median Itemizing Value YoY | Median Itemizing Value per Sq. Ft. YoY | Median Itemizing Value vs February 2019 | Median Itemizing Value per Sq. Ft. vs February 2019 |

| Atlanta-Sandy Springs-Roswell, Ga. | 1.8% | $398,894 | -2.7% | -1.3% | 24.8% | 55.9% |

| Austin-Round Rock-San Marcos, Texas | 1.0% | $499,000 | -7.9% | -5.9% | 42.6% | 54.3% |

| Baltimore-Columbia-Towson, Md. | 3.7% | $350,000 | 6.2% | 2.0% | 16.7% | 28.5% |

| Birmingham, Ala. | 1.8% | $285,000 | 0.3% | 0.5% | 20.3% | 33.6% |

| Boston-Cambridge-Newton, Mass.-N.H. | 1.4% | $839,450 | -1.8% | 1.6% | 52.8% | 73.6% |

| Buffalo-Cheektowaga, N.Y. | 2.0% | $249,974 | -0.5% | 1.1% | 37.0% | 52.7% |

| Charlotte-Concord-Gastonia, N.C.-S.C. | 0.8% | $419,475 | 4.9% | 1.3% | 27.2% | 62.2% |

| Chicago-Naperville-Elgin, Ill.-Ind. | 1.2% | $349,450 | -2.9% | -0.3% | 11.9% | 30.2% |

| Cincinnati, Ohio-Ky.-Ind. | 1.4% | $324,950 | -3.7% | 2.2% | 28.0% | 54.6% |

| Cleveland, Ohio | 2.0% | $241,725 | 14.0% | 14.9% | 34.3% | 60.1% |

| Columbus, Ohio | 1.4% | $349,700 | -7.2% | 1.6% | 29.9% | 59.9% |

| Dallas-Fort Worth-Arlington, Texas | 1.2% | $415,950 | -4.4% | -0.6% | 19.7% | 43.6% |

| Denver-Aurora-Centennial, Colo. | 1.8% | $572,500 | -6.1% | -3.0% | 14.6% | 44.3% |

| Detroit-Warren-Dearborn, Mich. | 1.5% | $239,900 | 4.6% | 2.9% | 9.1% | 26.9% |

| Grand Rapids-Wyoming-Kentwood, Mich. | 0.6% | $384,725 | -6.2% | -2.3% | 39.1% | 52.6% |

| Hartford-West Hartford-East Hartford, Conn. | 0.9% | $433,700 | 6.6% | 12.4% | 48.4% | 61.8% |

| Houston-Pasadena-The Woodlands, Texas | 1.0% | $358,000 | -0.5% | -1.0% | 15.5% | 37.6% |

| Indianapolis-Carmel-Greenwood, Ind. | 1.8% | $300,000 | -5.8% | 0.1% | 16.6% | 52.8% |

| Jacksonville, Fla. | 2.5% | $388,098 | -5.3% | -3.3% | 29.4% | 51.1% |

| Kansas City, Mo.-Kan. | 2.6% | $379,450 | -9.9% | -0.9% | 21.4% | 44.2% |

| Las Vegas-Henderson-North Las Vegas, Nev. | 1.3% | $469,974 | 1.1% | 3.0% | 51.2% | 58.0% |

| Los Angeles-Long Beach-Anaheim, Calif. | 0.9% | $1,119,000 | -1.6% | 1.4% | 49.3% | 55.1% |

| Louisville/Jefferson County, Ky.-Ind. | 1.6% | $309,950 | -0.3% | 1.6% | 20.2% | 44.7% |

| Memphis, Tenn.-Miss.-Ark. | 2.8% | $328,050 | 1.3% | 2.7% | 59.4% | 69.8% |

| Miami-Fort Lauderdale-West Palm Beach, Fla. | 1.2% | $515,000 | -6.4% | -5.1% | 32.1% | 48.4% |

| Milwaukee-Waukesha, Wis. | 1.3% | $374,950 | 6.4% | 6.8% | 43.2% | 54.4% |

| Minneapolis-St. Paul-Bloomington, Minn.-Wis. | 1.1% | $434,950 | 0.1% | -0.6% | 11.6% | 28.4% |

| Nashville-Davidson-Murfreesboro-Franklin, Tenn. | 1.5% | $529,450 | -5.4% | -1.0% | 47.4% | 63.3% |

| New York-Newark-Jersey City, N.Y.-N.J. | 1.1% | $766,889 | 1.9% | -2.4% | 39.6% | 79.4% |

| Oklahoma City, Okla. | 4.2% | $314,992 | -2.6% | 1.3% | 33.5% | 47.2% |

| Orlando-Kissimmee-Sanford, Fla. | 1.2% | $418,950 | -3.7% | -2.4% | 39.0% | 54.2% |

| Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | 1.8% | $350,000 | 3.0% | 4.4% | 40.0% | 59.4% |

| Phoenix-Mesa-Chandler, Ariz. | 1.0% | $515,000 | -4.9% | -1.0% | 47.2% | 59.3% |

| Pittsburgh, Pa. | 1.7% | $229,000 | 0.9% | 2.3% | 37.1% | 38.0% |

| Portland-Vancouver-Hillsboro, Ore.-Wash. | 1.4% | $598,415 | -0.3% | -0.6% | 25.2% | 40.0% |

| Providence-Warwick, R.I.-Mass. | 1.4% | $534,900 | 7.0% | 7.8% | 49.7% | 52.7% |

| Raleigh-Cary, N.C. | 0.9% | $435,962 | -1.5% | 0.4% | 22.9% | 54.7% |

| Richmond, Va. | 2.7% | $429,653 | -4.2% | 2.3% | 34.5% | 59.8% |

| Riverside-San Bernardino-Ontario, Calif. | 1.0% | $599,450 | 0.7% | 0.8% | 49.9% | 59.9% |

| Sacramento-Roseville-Folsom, Calif. | 1.3% | $619,000 | -2.2% | -1.3% | 34.0% | 39.0% |

| San Antonio-New Braunfels, Texas | 3.0% | $327,000 | -2.4% | -2.1% | 14.4% | 36.6% |

| San Diego-Chula Vista-Carlsbad, Calif. | 3.1% | $949,995 | -4.7% | -2.0% | 42.0% | 62.4% |

| San Francisco-Oakland-Fremont, Calif. | 1.2% | $899,944 | -9.0% | -7.3% | 1.5% | 17.9% |

| San Jose-Sunnyvale-Santa Clara, Calif. | 1.0% | $1,304,500 | -4.6% | 0.2% | 19.1% | 21.4% |

| Seattle-Tacoma-Bellevue, Wash. | 1.5% | $737,400 | -3.6% | 0.9% | 24.2% | 54.0% |

| St. Louis, Mo.-Ill. | 1.8% | $276,799 | -3.7% | -2.8% | 31.8% | 31.0% |

| Tampa-St. Petersburg-Clearwater, Fla. | 2.0% | $399,000 | -4.0% | -4.0% | 47.8% | 64.2% |

| Tucson, Ariz. | 2.8% | $396,200 | -1.0% | -1.2% | 38.7% | 55.7% |

| Virginia Beach-Chesapeake-Norfolk, Va.-N.C. | 7.0% | $392,500 | 1.4% | 5.4% | 41.7% | 53.9% |

| Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | 11.0% | $579,995 | -3.3% | 0.0% | 28.9% | 58.4% |

Supply: U.S. Bureau of Labor Statistics, State and Space Employment, Hours, and Earnings, Employed and Workplace of Employment and Unemployment Statistics : Authorities – Federal Authorities

| Metro Space | Lively Itemizing Depend YoY | New Itemizing Depend YoY | Median Days on Market | Median Days on Market Y-Y (Days) | Value– Lowered Share | Value-Lowered Share Y-Y (Proportion Factors) |

| Atlanta-Sandy Springs-Roswell, Ga. | 40.9% | 7.1% | 58 | 16 | 20.5% | 5.1 pp |

| Austin-Round Rock-San Marcos, Texas | 19.6% | 1.7% | 66 | 6 | 20.2% | -0.6 pp |

| Baltimore-Columbia-Towson, Md. | 30.5% | 3.5% | 41 | -3 | 12.8% | 1.4 pp |

| Birmingham, Ala. | 17.2% | 6.4% | 71 | 5 | 15.0% | 1.7 pp |

| Boston-Cambridge-Newton, Mass.-N.H. | 11.7% | -2.8% | 33 | 0 | 9.5% | 1.7 pp |

| Buffalo-Cheektowaga, N.Y. | 25.2% | -20.0% | 79 | 13 | 6.0% | 0.8 pp |

| Charlotte-Concord-Gastonia, N.C.-S.C. | 45.7% | 9.3% | 56 | 11 | 20.9% | 6.4 pp |

| Chicago-Naperville-Elgin, Ill.-Ind. | 9.0% | -0.1% | 43 | 2 | 10.4% | 1.5 pp |

| Cincinnati, Ohio-Ky.-Ind. | 25.4% | 9.5% | 50 | 11 | 14.0% | 3.1 pp |

| Cleveland, Ohio | 11.7% | -6.0% | 61 | 10 | 13.0% | 1.8 pp |

| Columbus, Ohio | 34.8% | 4.3% | 49 | 12 | 18.4% | 2.6 pp |

| Dallas-Fort Worth-Arlington, Texas | 36.1% | 0.2% | 56 | 9 | 22.0% | 2.8 pp |

| Denver-Aurora-Centennial, Colo. | 64.4% | 20.1% | 44 | 10 | 22.9% | 8.0 pp |

| Detroit-Warren-Dearborn, Mich. | 6.2% | -8.3% | 52 | 6 | 11.1% | -0.3 pp |

| Grand Rapids-Wyoming-Kentwood, Mich. | 29.8% | 5.2% | 56 | 5 | 10.7% | 2.9 pp |

| Hartford-West Hartford-East Hartford, Conn. | 4.4% | -1.7% | 38 | -3 | 6.0% | -0.1 pp |

| Houston-Pasadena-The Woodlands, Texas | 28.1% | 8.8% | 54 | 6 | 17.6% | 0.9 pp |

| Indianapolis-Carmel-Greenwood, Ind. | 22.8% | 0.3% | 63 | 4 | 19.6% | 3.9 pp |

| Jacksonville, Fla. | 36.8% | -3.7% | 66 | 16 | 26.6% | 5.8 pp |

| Kansas City, Mo.-Kan. | 11.4% | -4.2% | 75 | 3 | 10.7% | -0.1 pp |

| Las Vegas-Henderson-North Las Vegas, Nev. | 60.8% | 19.7% | 47 | 8 | 19.2% | 5.7 pp |

| Los Angeles-Long Beach-Anaheim, Calif. | 43.0% | 27.1% | 39 | -1 | 11.8% | 2.9 pp |

| Louisville/Jefferson County, Ky.-Ind. | 19.8% | -3.1% | 51 | 4 | 17.0% | 2.6 pp |

| Memphis, Tenn.-Miss.-Ark. | 29.1% | -2.0% | 71 | 4 | 19.2% | 1.0 pp |

| Miami-Fort Lauderdale-West Palm Beach, Fla. | 39.2% | 7.1% | 74 | 12 | 20.6% | 1.0 pp |

| Milwaukee-Waukesha, Wis. | 11.1% | 24.3% | 36 | -1 | 11.3% | 1.2 pp |

| Minneapolis-St. Paul-Bloomington, Minn.-Wis. | 8.8% | -6.3% | 41 | 4 | 9.8% | 1.3 pp |

| Nashville-Davidson-Murfreesboro-Franklin, Tenn. | 30.8% | 12.9% | 55 | 16 | 16.0% | -1.4 pp |

| New York-Newark-Jersey City, N.Y.-N.J. | 1.0% | 0.0% | 68 | -1 | 5.9% | -0.6 pp |

| Oklahoma City, Okla. | 34.2% | 5.1% | 52 | -4 | 17.0% | -1.1 pp |

| Orlando-Kissimmee-Sanford, Fla. | 43.8% | 17.1% | 74 | 10 | 23.3% | 3.6 pp |

| Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | 14.6% | -3.4% | 52 | -7 | 11.8% | 0.8 pp |

| Phoenix-Mesa-Chandler, Ariz. | 45.3% | 14.7% | 56 | 11 | 30.2% | 5.2 pp |

| Pittsburgh, Pa. | 13.7% | -10.1% | 86 | 9 | 14.2% | -0.2 pp |

| Portland-Vancouver-Hillsboro, Ore.-Wash. | 24.8% | -2.0% | 75 | 21 | 22.5% | 3.5 pp |

| Providence-Warwick, R.I.-Mass. | 20.2% | -3.0% | 39 | 1 | 8.7% | 1.9 pp |

| Raleigh-Cary, N.C. | 41.6% | 6.2% | 53 | 9 | 15.7% | 3.5 pp |

| Richmond, Va. | 16.9% | -5.1% | 49 | 1 | 10.5% | 1.6 pp |

| Riverside-San Bernardino-Ontario, Calif. | 47.2% | 17.8% | 60 | 10 | 17.0% | 4.0 pp |

| Sacramento-Roseville-Folsom, Calif. | 45.4% | 20.9% | 39 | 0 | 13.4% | 3.0 pp |

| San Antonio-New Braunfels, Texas | 15.1% | 0.2% | 76 | 8 | 24.7% | 3.5 pp |

| San Diego-Chula Vista-Carlsbad, Calif. | 61.3% | 24.3% | 34 | 1 | 14.6% | 4.0 pp |

| San Francisco-Oakland-Fremont, Calif. | 34.0% | 27.2% | 30 | 2 | 9.4% | 1.9 pp |

| San Jose-Sunnyvale-Santa Clara, Calif. | 46.1% | 28.0% | 22 | -1 | 7.3% | 2.2 pp |

| Seattle-Tacoma-Bellevue, Wash. | 40.8% | 4.2% | 35 | 3 | 11.2% | 3.9 pp |

| St. Louis, Mo.-Ill. | 13.8% | 3.8% | 53 | 5 | 12.7% | 2.2 pp |

| Tampa-St. Petersburg-Clearwater, Fla. | 28.9% | 3.9% | 66 | 9 | 27.5% | 2.0 pp |

| Tucson, Ariz. | 47.4% | 8.9% | 52 | 8 | 24.1% | 6.3 pp |

| Virginia Beach-Chesapeake-Norfolk, Va.-N.C. | 27.2% | 1.9% | 39 | 3 | 16.0% | 1.0 pp |

| Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | 41.0% | 8.5% | 34 | -3 | 10.8% | 2.3 pp |

Methodology

Realtor.com housing information as of February 2025. Listings embrace the lively stock of current single-family houses and condos/townhomes/row houses/co-ops for the given degree of geography on Realtor.com; new building is excluded until listed by way of an MLS that gives itemizing information to Realtor.com. Realtor.com information historical past goes again to July 2016. The 50 largest U.S. metropolitan areas as outlined by the Workplace of Administration and Finances (OMB-202301) and Claritas 2025 estimates of family counts. With the discharge of its January 2025 housing developments report, Realtor.com® has restated information factors for some earlier months. Because of these modifications, a number of the information launched since January 2025 won’t be straight comparable with earlier information releases (recordsdata downloaded earlier than January 2025) and Realtor.com® economics analysis reviews.