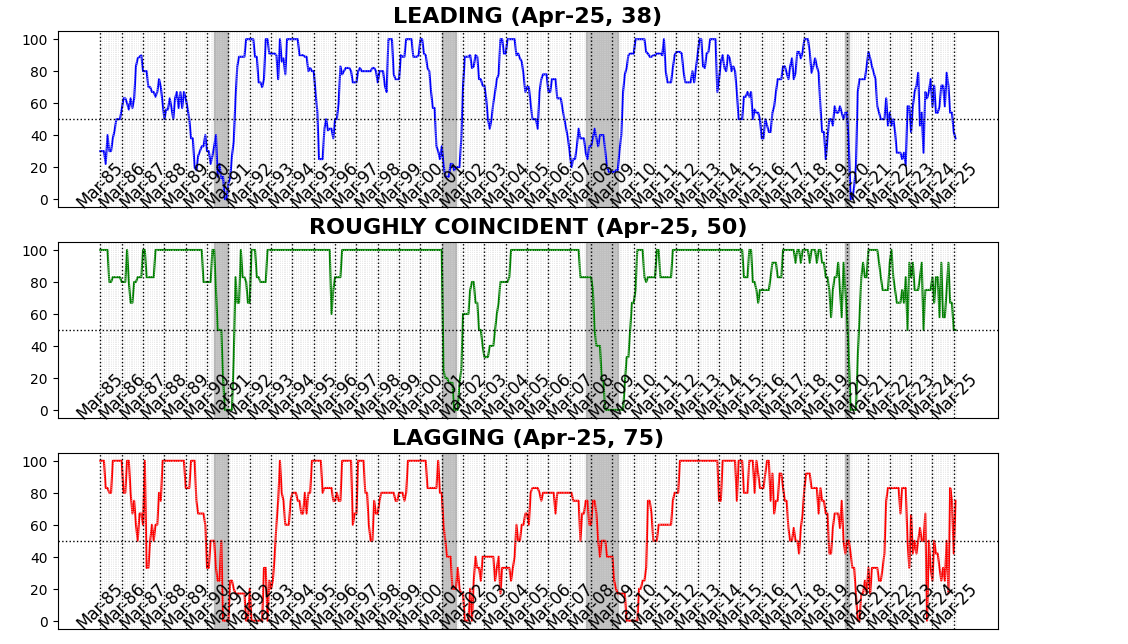

AIER’s Enterprise Situations Month-to-month indicators counsel that the US economic system remained below strain in April, with the Main Indicator slipping additional into contractionary territory. After March’s sharp 12-point drop, the Main Indicator declined an extra 4 factors in April, touchdown at 38 — its lowest studying since October 2023 and an indication that forward-looking financial momentum continues to erode.

The Roughly Coincident Indicator held regular at 50, matching its March degree. Whereas this impartial studying could seem secure on the floor, it masks the underlying lack of tempo that adopted a string of stronger readings earlier within the yr. The Lagging Indicator, against this, rebounded strongly — leaping 33 factors to 75 — erasing its March plunge and signaling that backward-looking measures corresponding to credit score delinquencies and enterprise debt service stay comparatively agency, at the least for now. However such lags are typical in financial slowdowns and don’t alter the broader image of softening circumstances throughout ahead and present-focused metrics.

Main Indicator (38)

In April, the Main Indicator fell additional to 38, down from 42 in March, marking its lowest studying since October 2023. The index mirrored weak point throughout the vast majority of parts, with solely 4 of twelve exhibiting enchancment and the remaining contributing negatively or remaining flat.

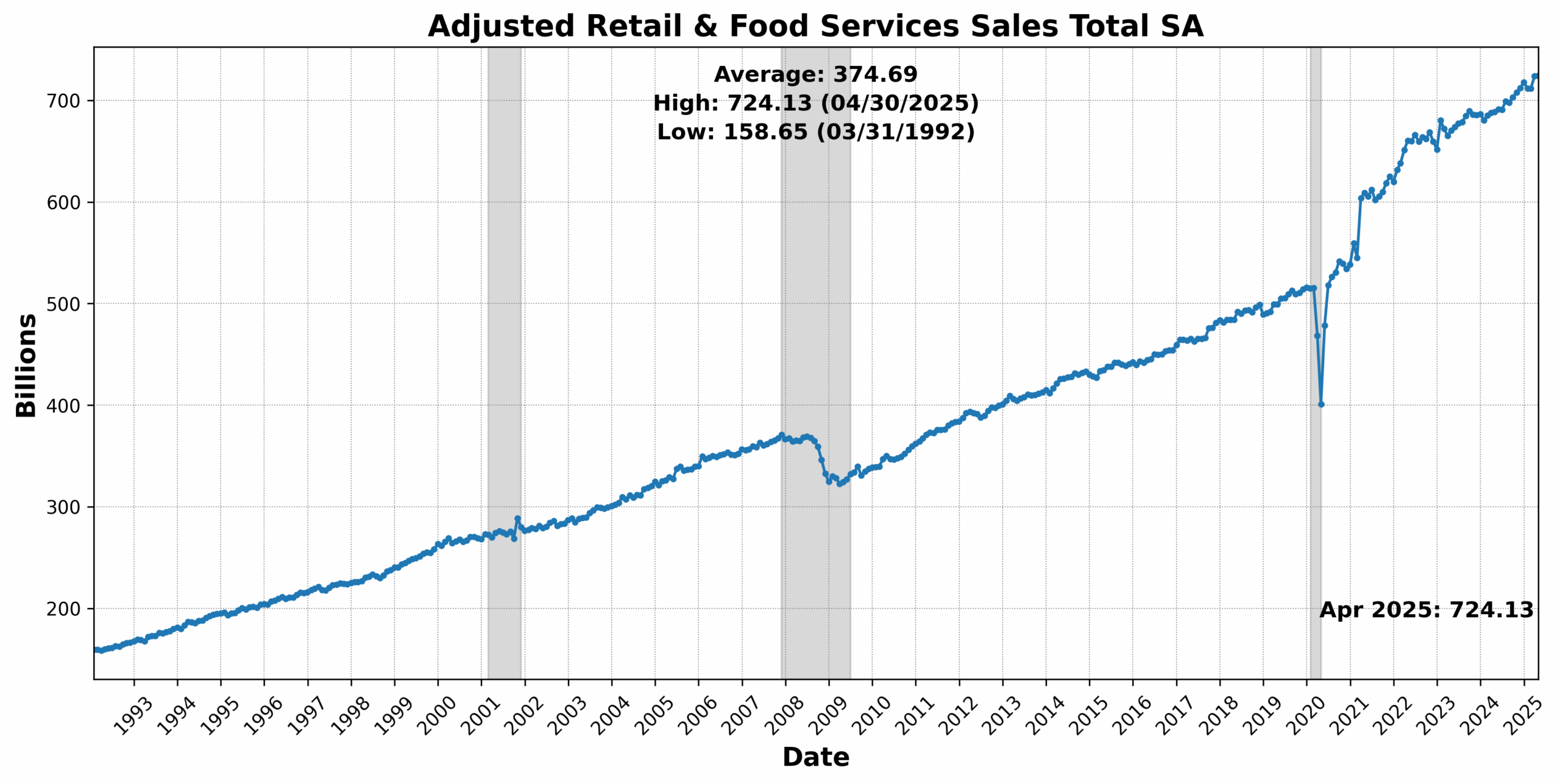

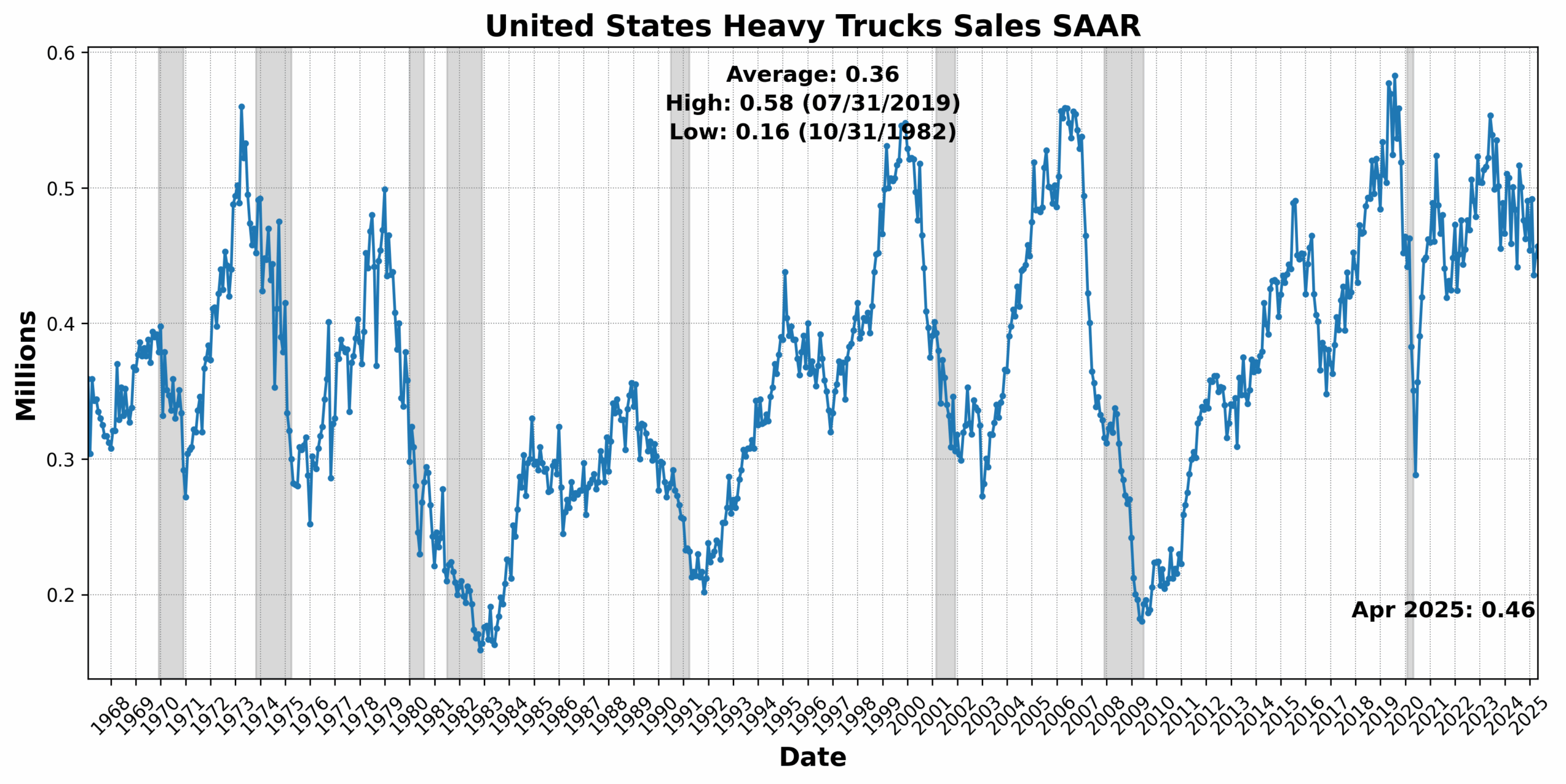

The strongest beneficial properties got here from the Convention Board US Main Index Producers’ New Orders: Client Items and Supplies, up 1.7 p.c, and US New Privately Owned Housing Items Began by Construction Whole SAAR, which rose 1.6 p.c — an indication that regardless of greater rates of interest, housing development stays resilient in some areas. United States Heavy Vans Gross sales SAAR additionally rose 1.6 p.c, probably reflecting fleet funding or elevated freight exercise. Adjusted Retail and Meals Providers Gross sales Whole seasonally adjusted (SA) posted a marginal acquire of 0.1 p.c, suggesting flat however secure client spending.

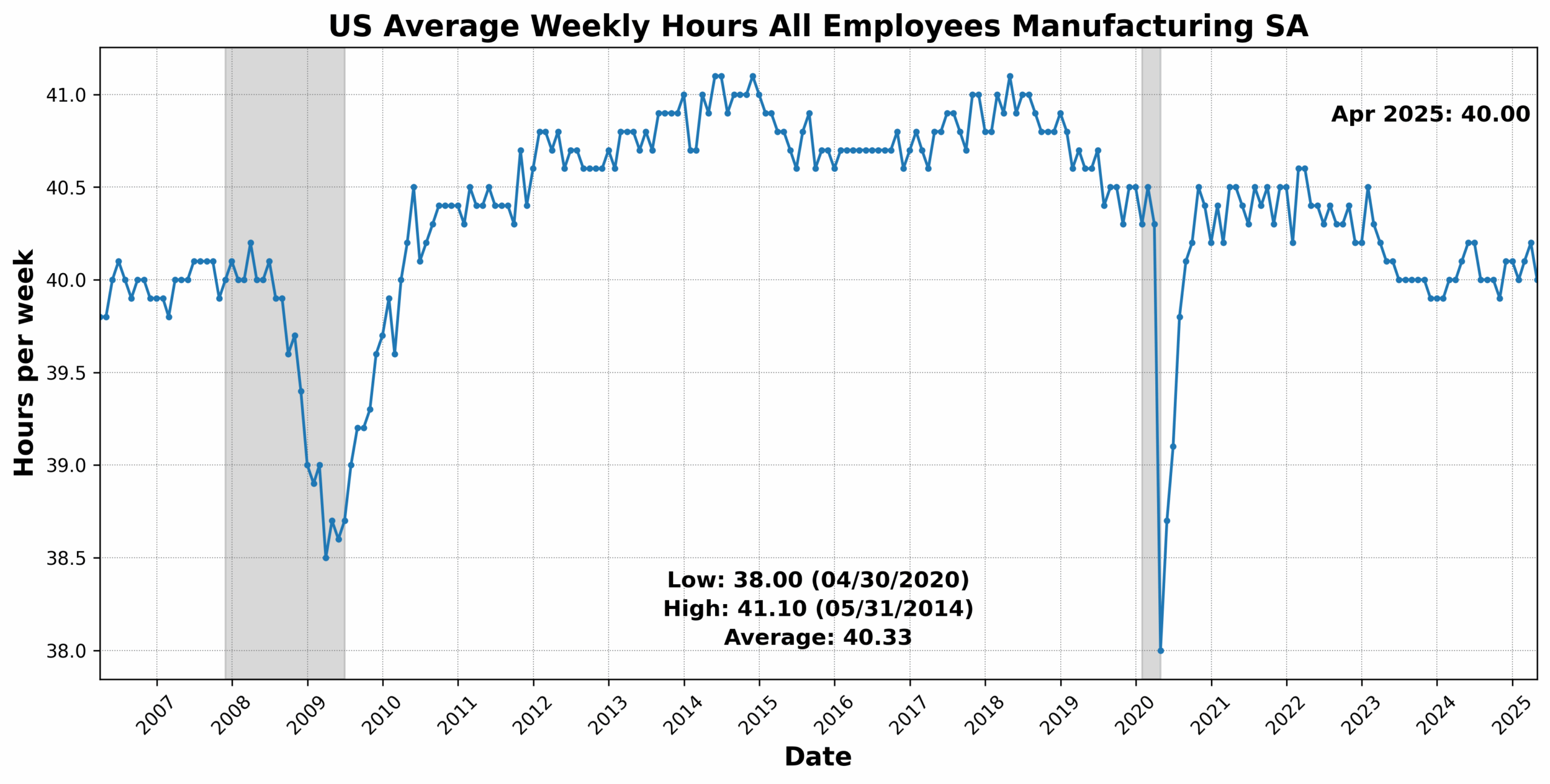

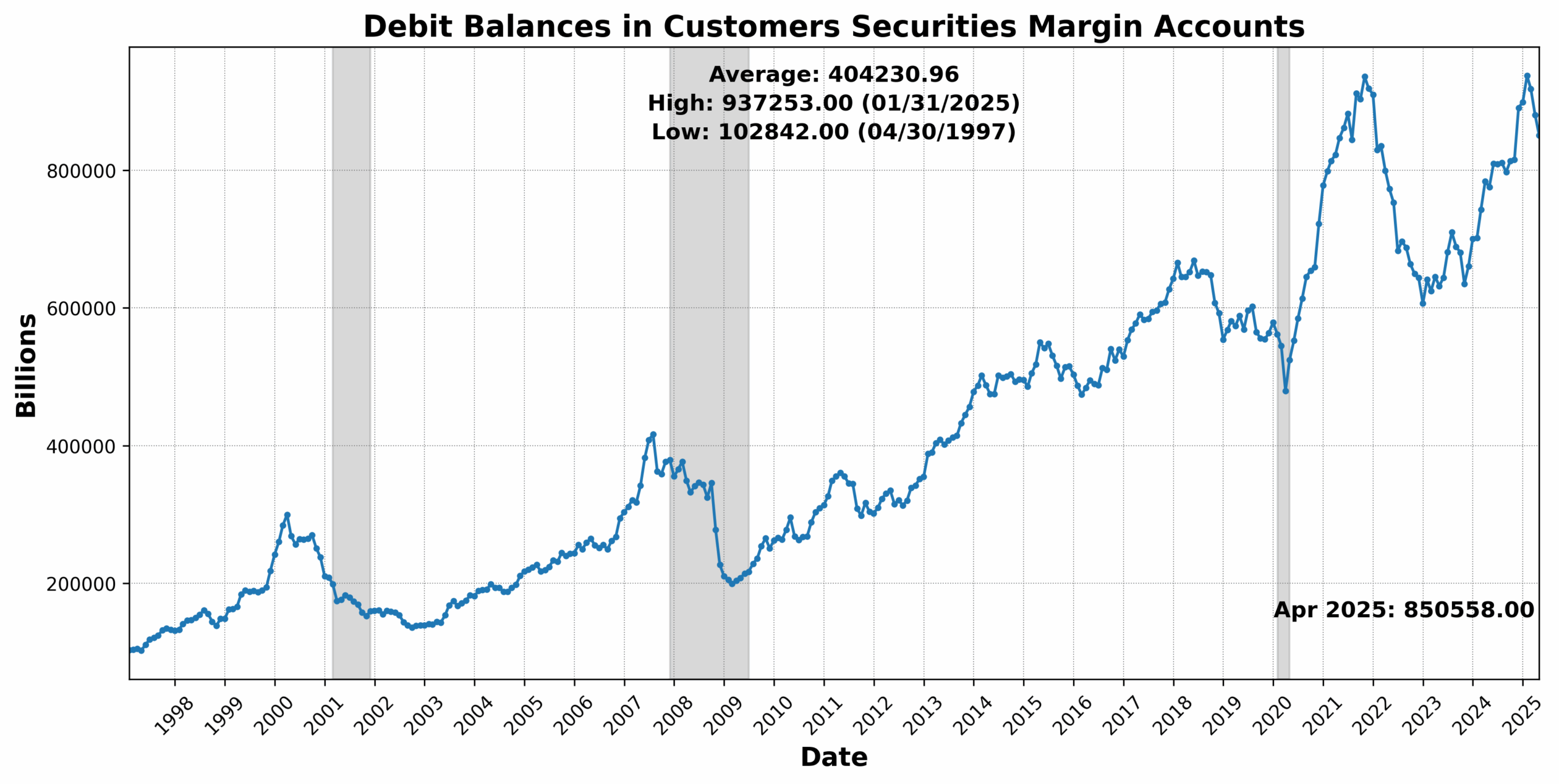

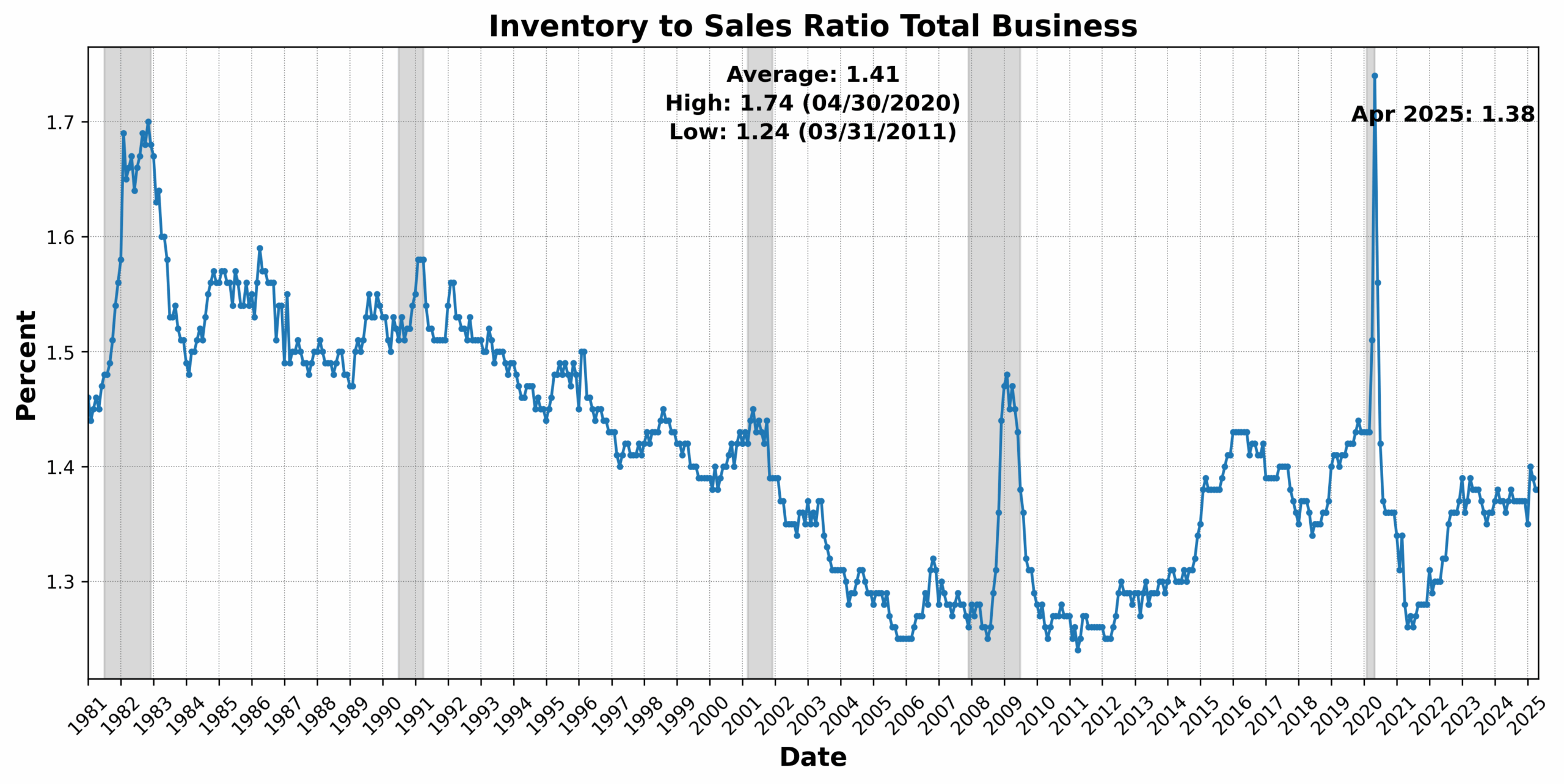

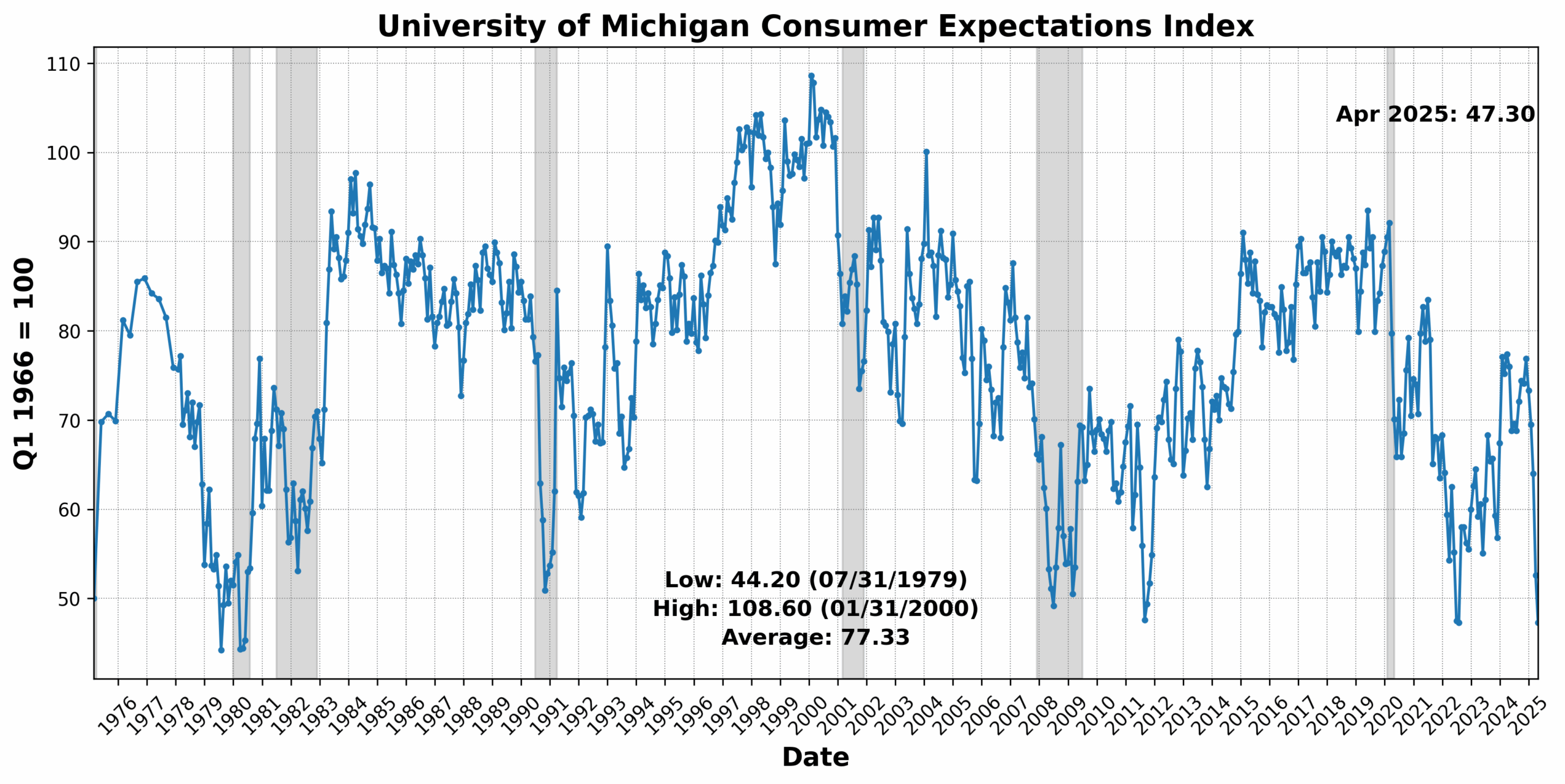

On the draw back, the College of Michigan Client Expectations Index dropped sharply by 10.1 p.c, signaling a weakening client outlook. US Preliminary Jobless Claims SA fell 10.0 p.c — often a optimistic signal — however on this context could mirror tightening labor circumstances which might be slowing momentum. Fairness costs (through the Convention Board US Main Index Inventory Costs 500 Frequent Shares) declined by 5.5 p.c, whereas Debit Balances in Prospects’ Securities Margin Accounts fell 3.4 p.c, pointing to decreased investor danger urge for food. Convention Board US Producers’ New Orders Nondefense Capital Items Ex Plane fell 1.1 p.c, and US Common Weekly Hours All Staff Manufacturing SA slipped 0.5 p.c — each early indicators of slowing industrial demand. The Treasury yield curve remained deeply inverted, with the 1-12 months to 10-12 months US Treasury Yield Unfold at -73.4 p.c, reinforcing recessionary indicators. One element, the Stock to Gross sales Ratio Whole Enterprise, was flat.

Altogether, the deterioration throughout a large swath of main parts underscores rising draw back dangers for the US economic system heading into mid-2025.

Roughly Coincident Indicator (50)

The Roughly Coincident Index remained unchanged at 50 in April, reinforcing the image of a plateauing economic system with little internet ahead momentum. Three of the six underlying indicators rose, whereas three declined — persevering with the pattern of blended however secure readings.

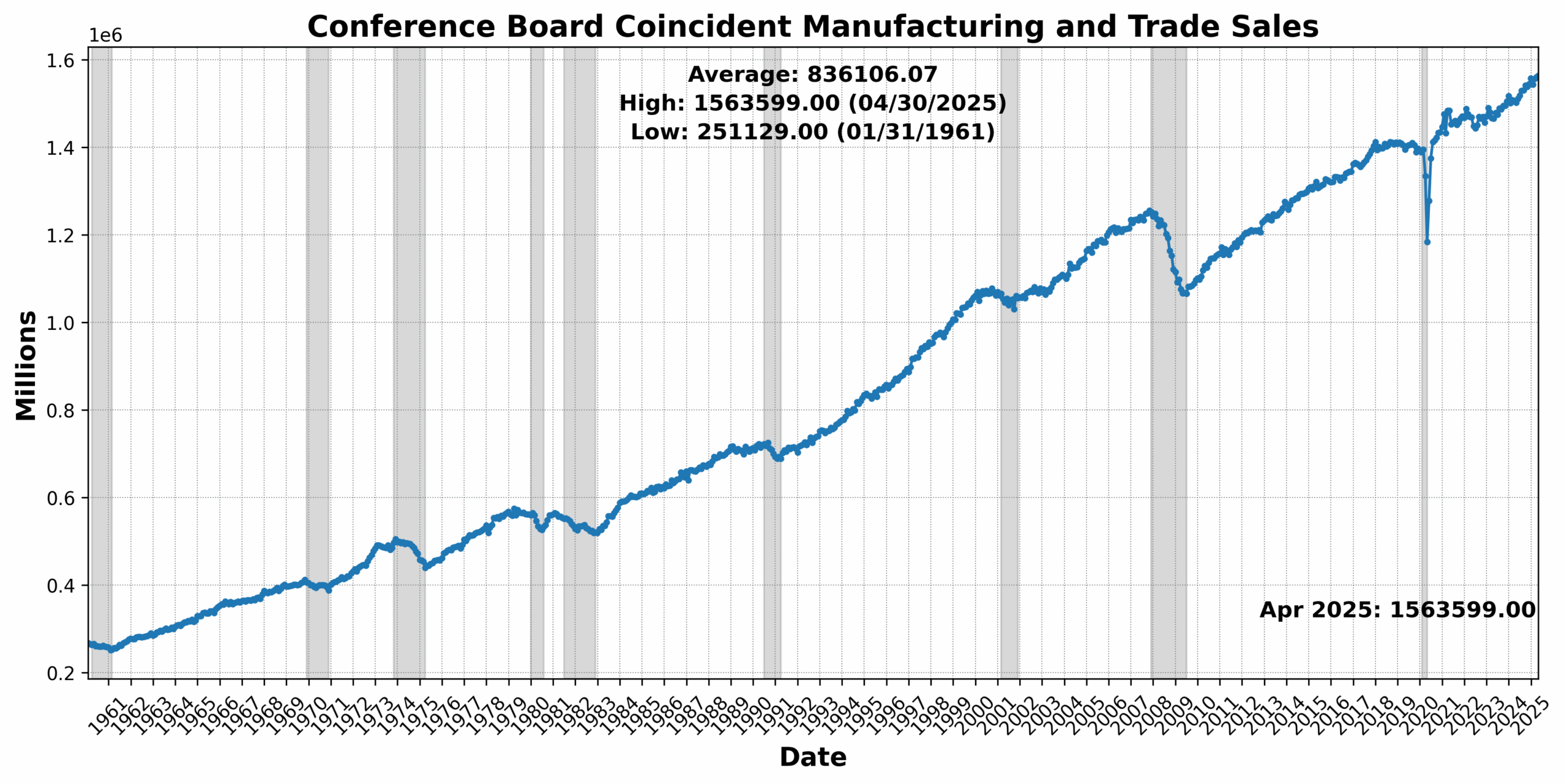

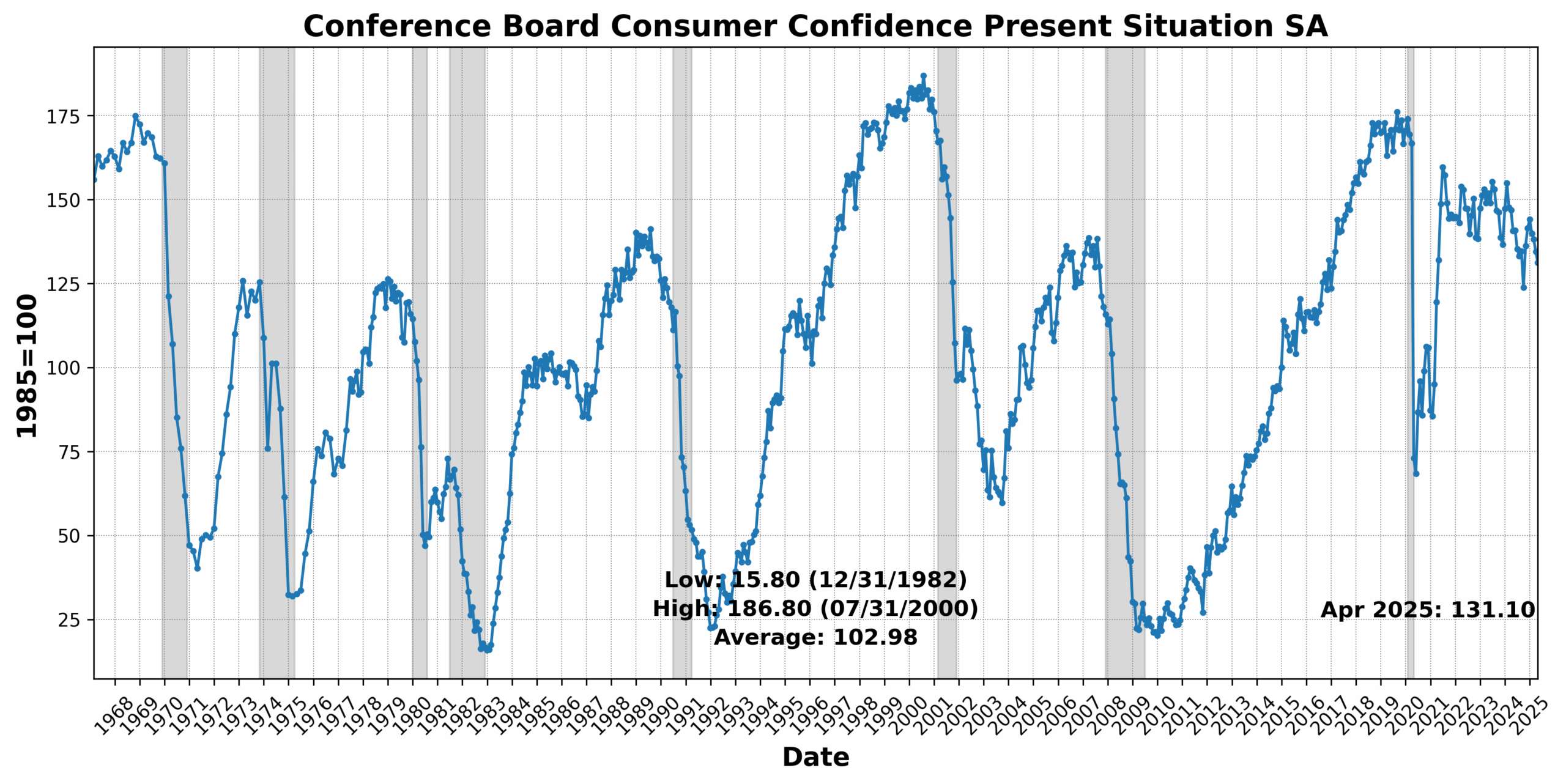

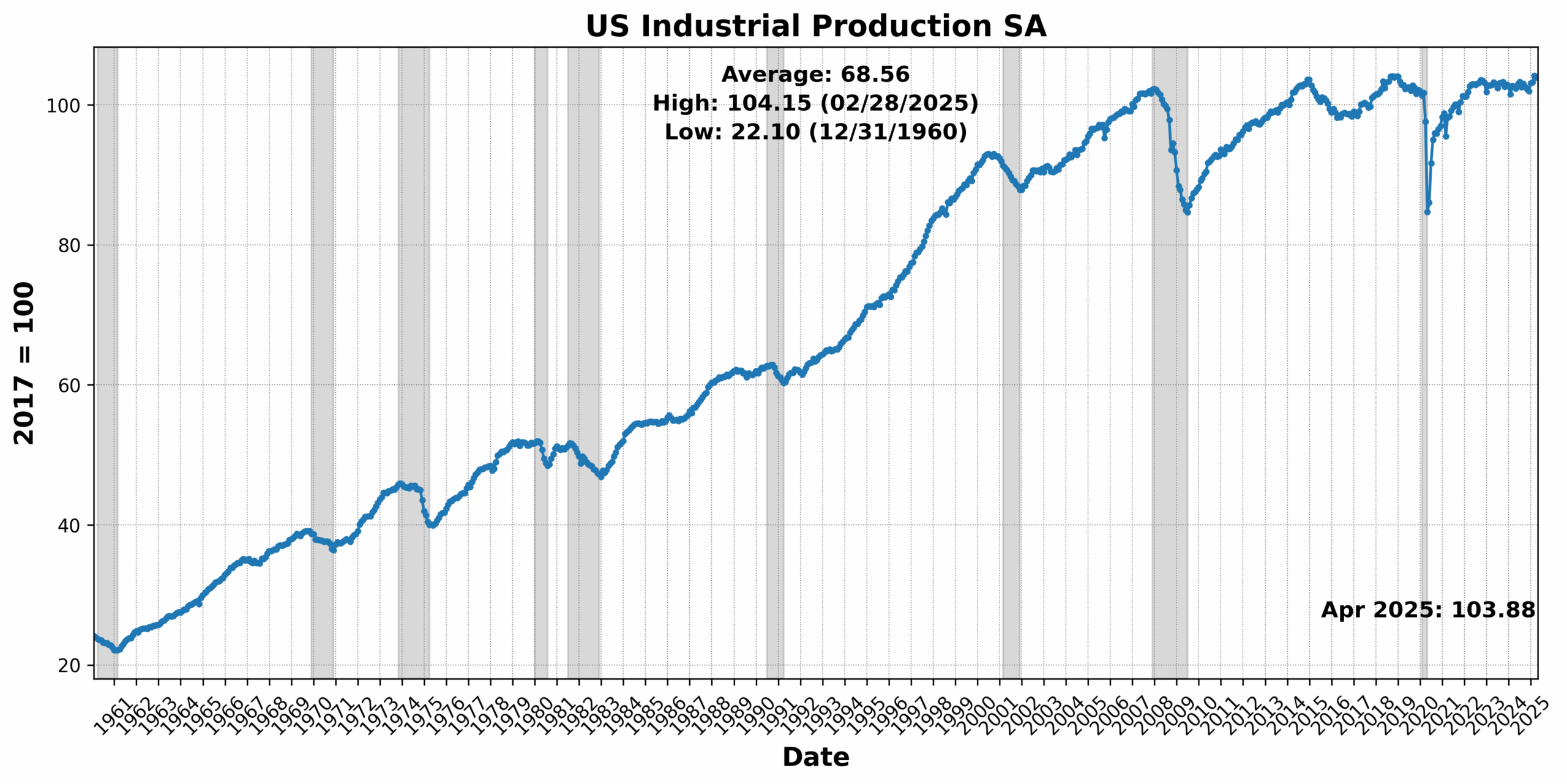

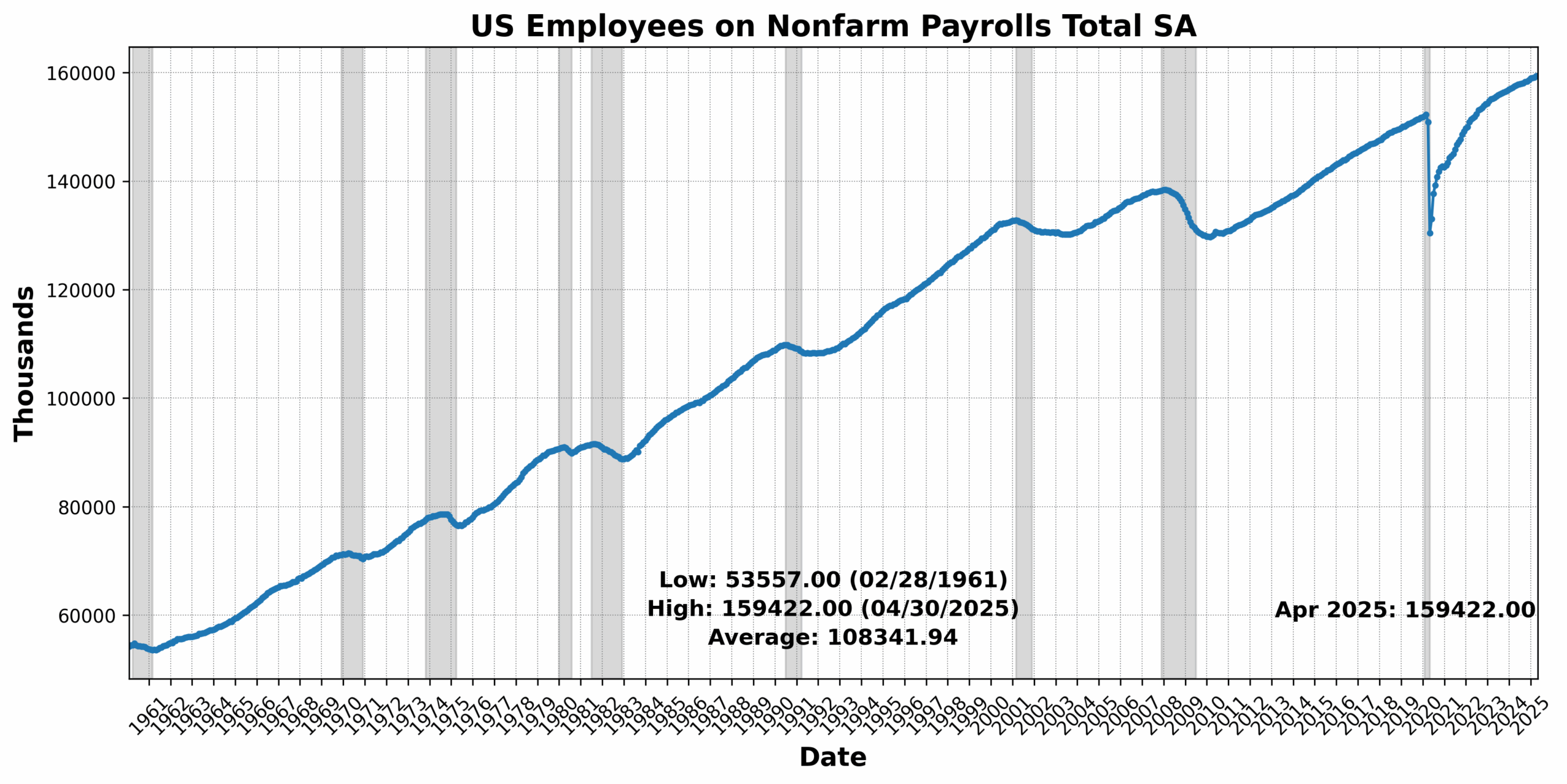

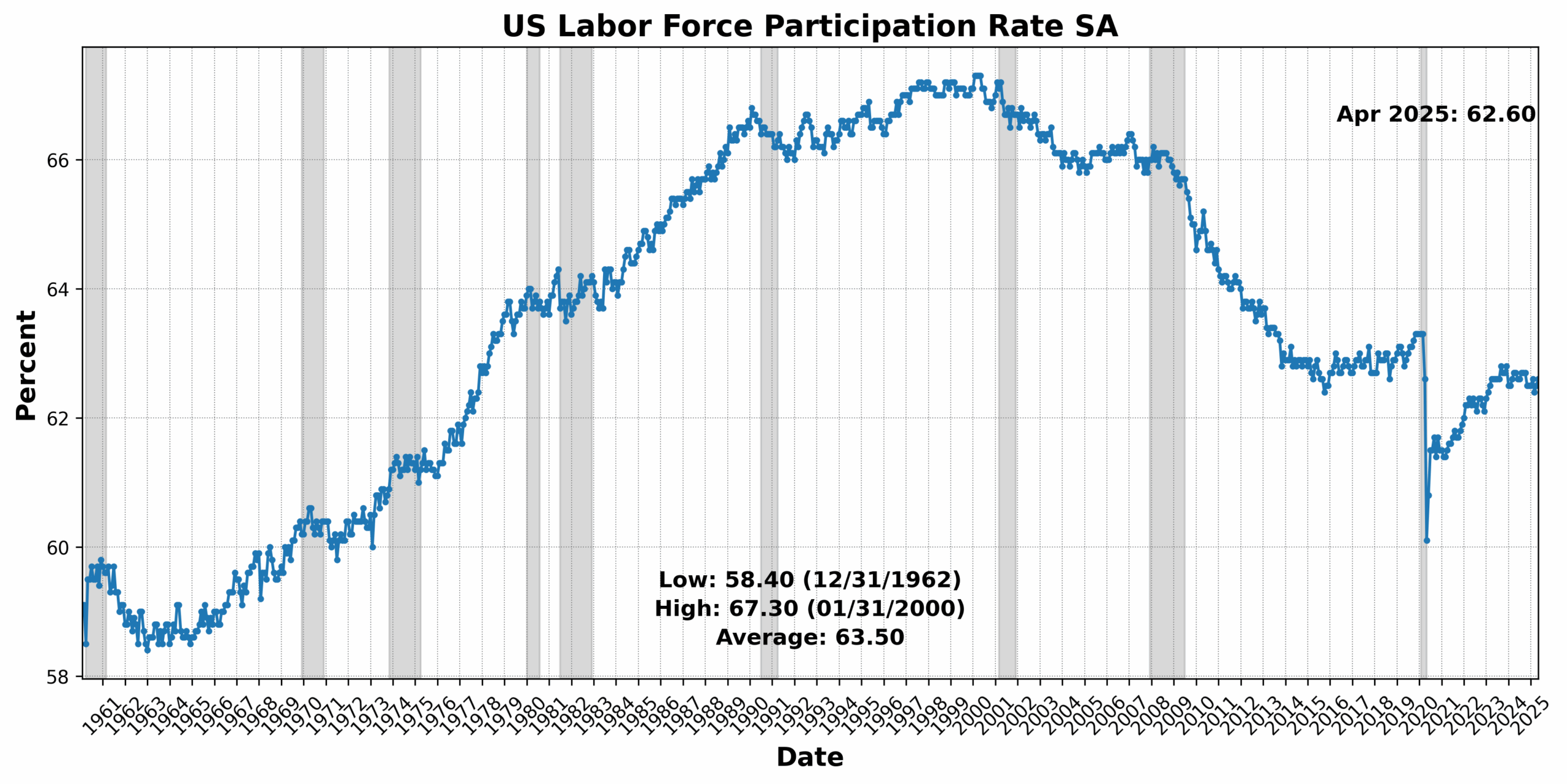

Convention Board Coincident Private Revenue Much less Switch Funds rose 0.5 p.c, suggesting some resilience in family earnings. Convention Board Coincident Manufacturing and Commerce Gross sales edged up 0.2 p.c, and US Staff on Nonfarm Payrolls Whole SA noticed a modest acquire of 0.1 p.c. Nevertheless, the US Labor Power Participation Fee SA slipped by 0.2 p.c, and US Industrial Manufacturing SA was primarily flat, down 0.0 p.c. The sharpest transfer got here from Convention Board Client Confidence Current State of affairs SA, which fell 2.5 p.c, highlighting persistent warning amongst households regardless of secure labor and earnings developments.

Lagging Indicator (75)

The Lagging Index rose sharply to 75 in April, up from 42 in March, pushed by broad-based beneficial properties throughout parts — with 5 of six exhibiting optimistic motion and just one declining.

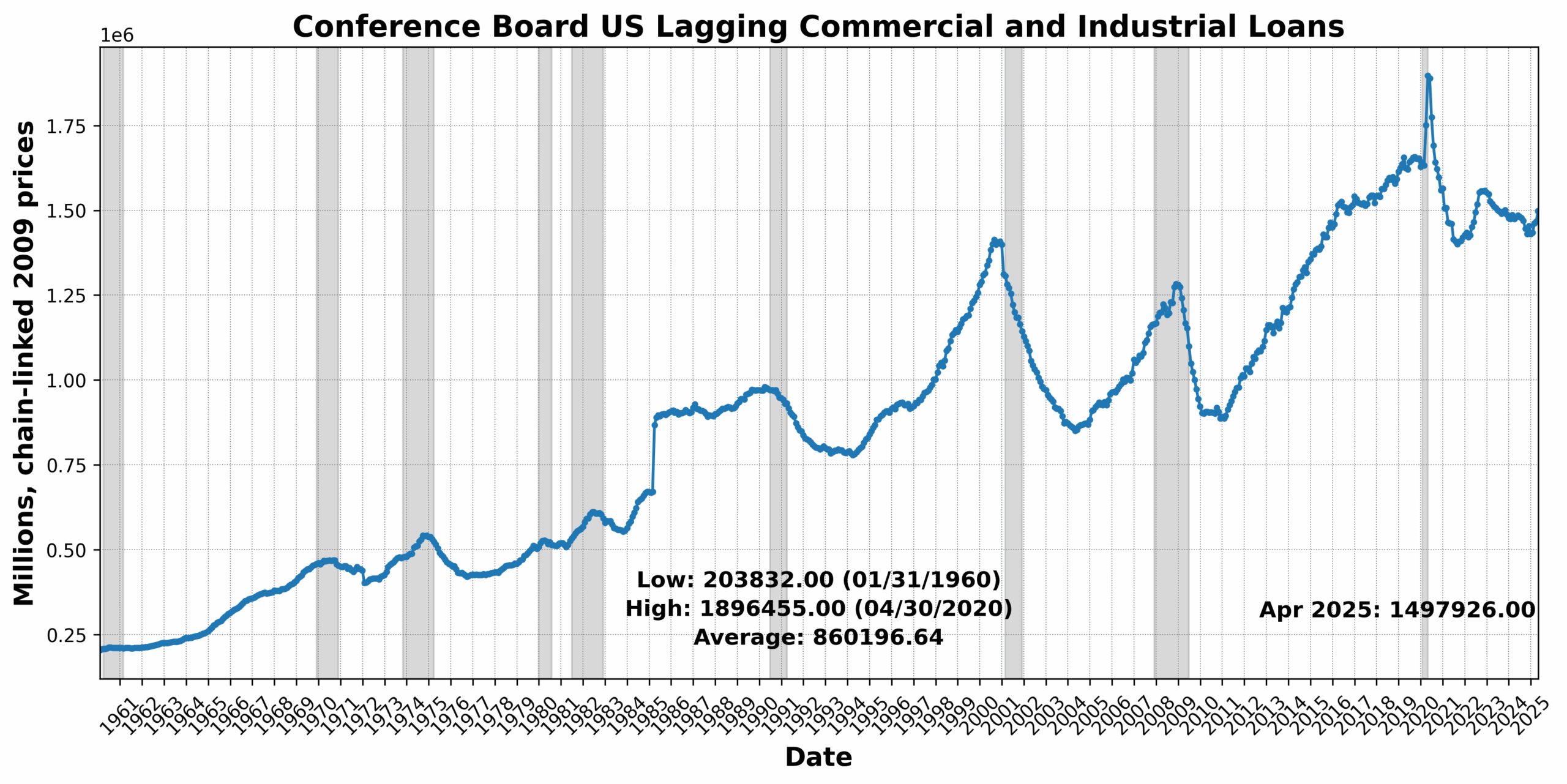

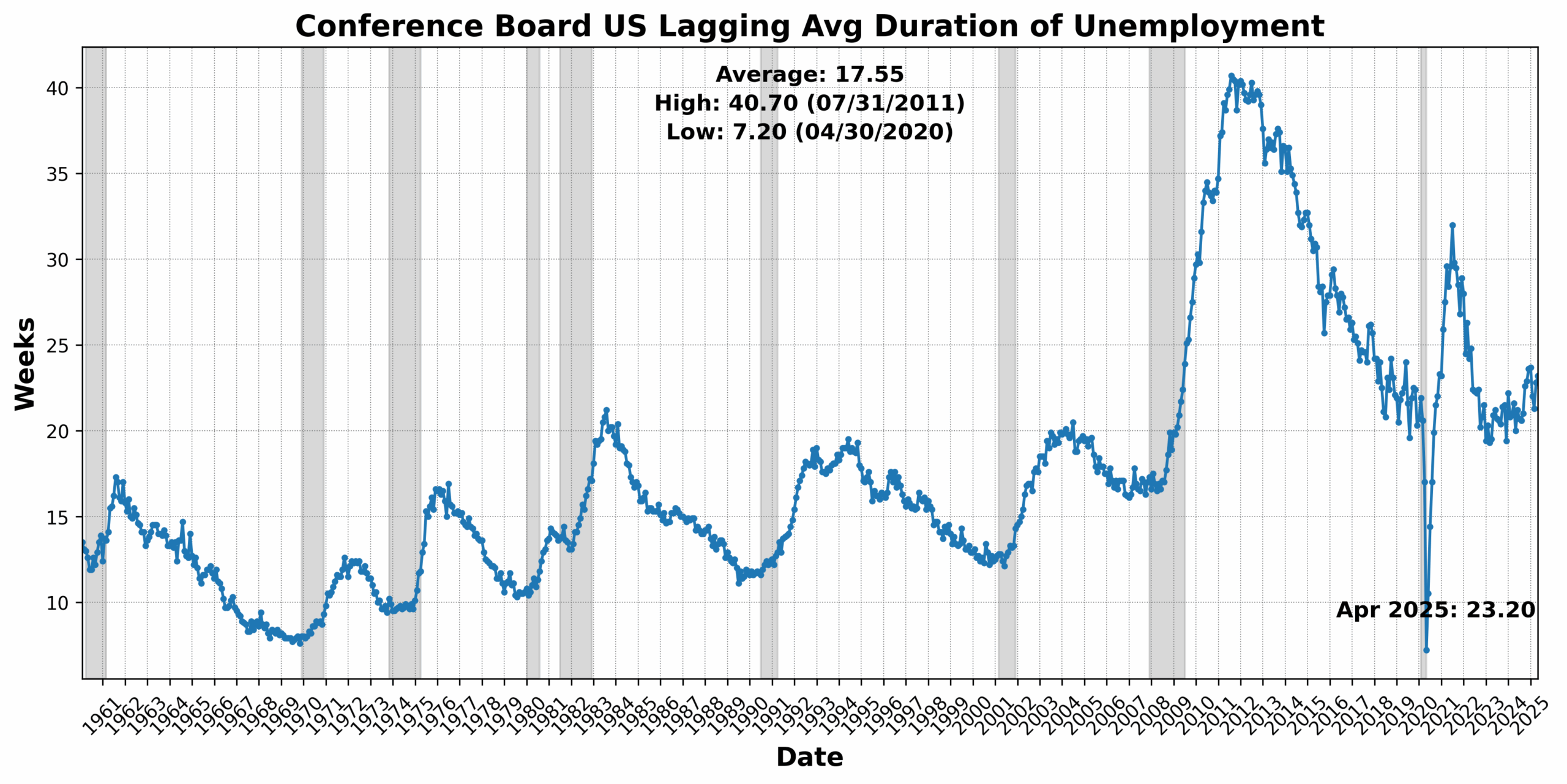

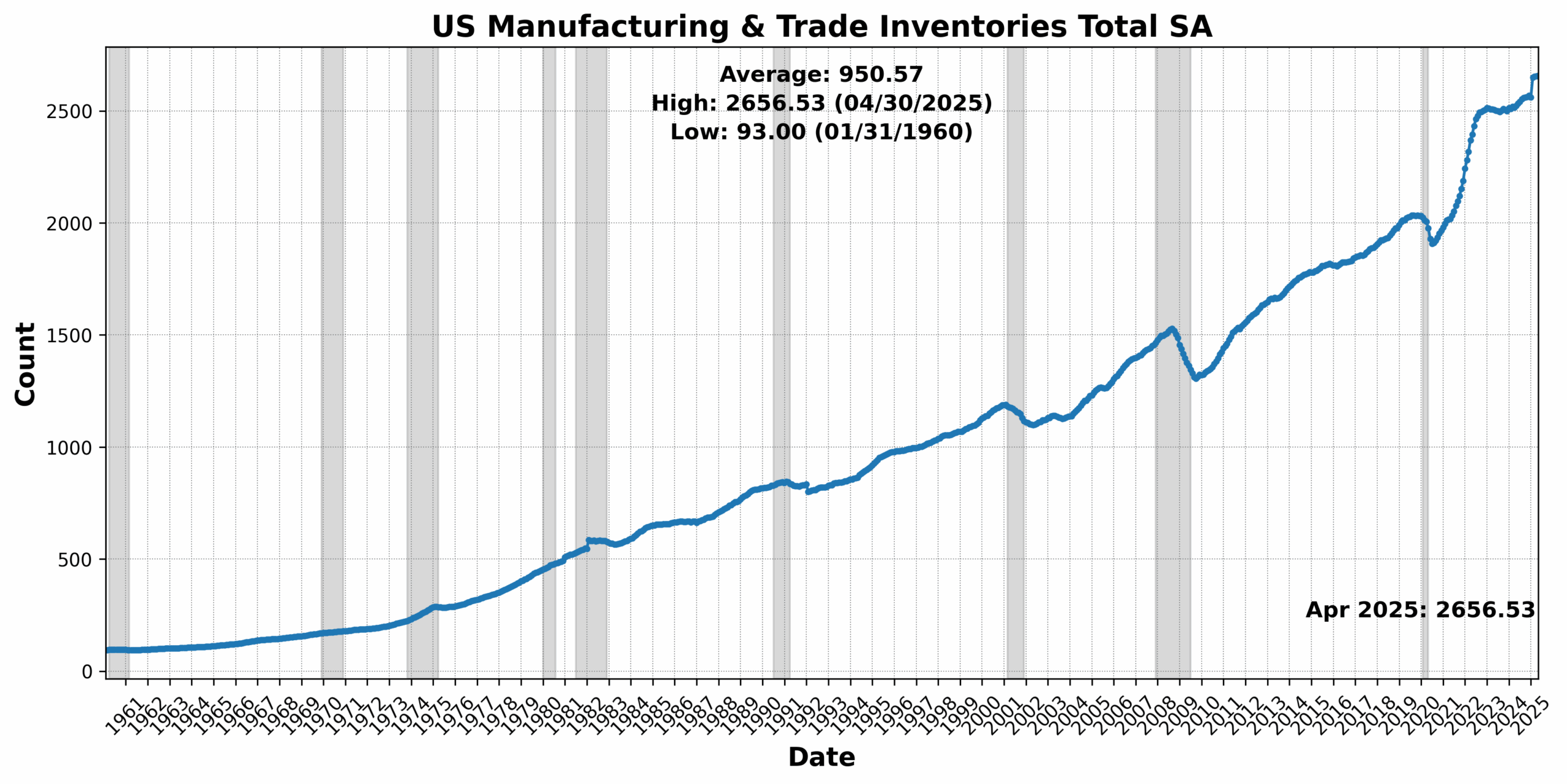

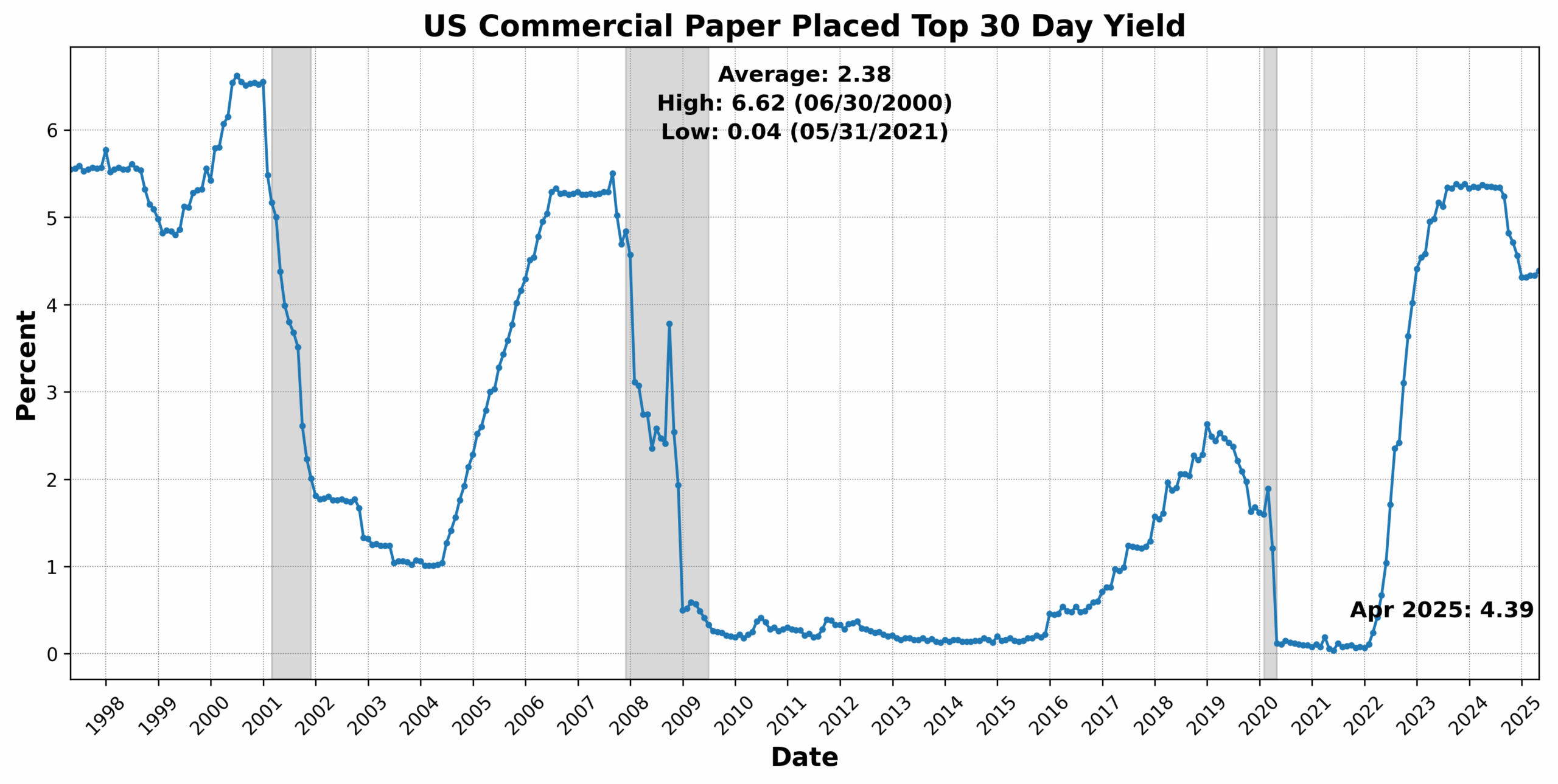

Convention Board US Lagging Business and Industrial Loans rose 2.1 p.c, whereas Convention Board US Lagging Avg Period of Unemployment elevated 1.8 p.c, pointing to a rising credit score extension but in addition an extended job-search cycle. US Business Paper Positioned High 30-Day Yield climbed 1.4 p.c, and US Manufacturing and Commerce Inventories Whole SA rose marginally. CPI for City Shoppers Much less Meals and Vitality, YoY NSA was unchanged, providing no disinflationary aid however no new inflation strain both. The lone drag got here from Census Bureau US Non-public Development Spending Nonresidential SA, which declined 0.9 p.c — a average pullback after earlier energy within the sector.

Altogether, the Lagging Index’s sturdy rebound displays late-cycle dynamics: greater credit score use, longer unemployment spells, and a firming of borrowing prices — according to a maturing, if not but reversing, enterprise cycle.

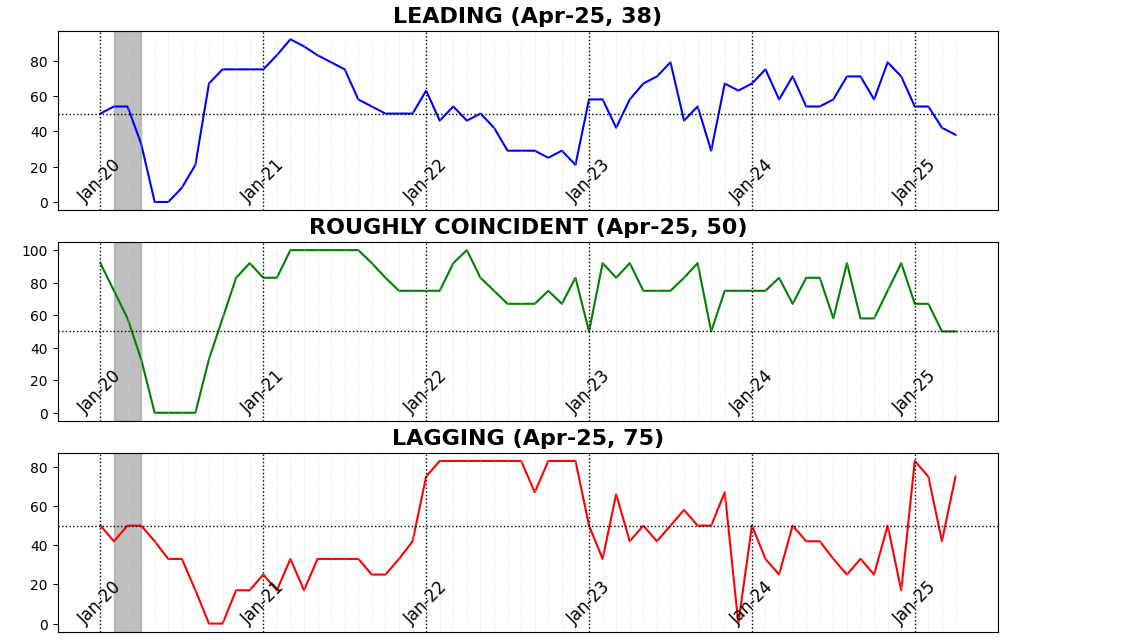

The trajectory of the AIER Enterprise Situations indicators over the previous yr tells a transparent story of fading momentum and rising financial uncertainty. Following a comparatively blended first half of 2024, November and December noticed a notable surge in each the Main and Roughly Coincident Indicators — probably reflecting optimism across the presidential election end result, with markets anticipating pro-growth or business-friendly insurance policies below a returning Trump administration.

Nevertheless, the sharp drop within the Lagging Indicator in December urged that longer-term circumstances, corresponding to credit score and price constructions, have been already below strain. After Trump’s inauguration in January 2025, the Main Indicator declined once more and has since continued its downward path, reaching simply 38 in April — the bottom studying since late 2023. This regular erosion probably displays mounting concern over the implications of the administration’s aggressive tariff posture, which by early April was being formally articulated however not but broadly applied. Whereas the Lagging Indicator has rebounded (reflecting greater credit score utilization and different late-cycle dynamics), the broader sample — of shrinking ahead momentum, regular however unremarkable coincident exercise, and an more and more heavy reliance on back-end financial help — suggests that companies and traders are rising cautious of near-term dangers. The honeymoon of post-election enthusiasm seems to have ended, and the economic system is now bracing for the real-world impression of rising commerce limitations and coverage volatility.

DISCUSSION, Could – June 2025

Could’s inflation knowledge paint a posh image of offsetting pressures inside the US economic system. Whereas each headline and core CPI readings got here in surprisingly comfortable — regardless of the onset of Trump’s overbroad tariffs — underlying particulars counsel vital tariff pass-through in items classes with excessive import publicity, notably main family home equipment and different sturdy items. Nevertheless, persistent deflation in classes like used automobiles, recreation providers, and portfolio administration charges helped offset upward strain, highlighting fragile client sentiment and uneven demand. Producer costs inform a extra regarding story: core items within the PPI report present accelerating inflation, notably in completed sturdy items, suggesting that corporations are absorbing enter value will increase and experiencing margin compression. This divergence between PPI and CPI implies that inflationary pressures could also be constructing beneath the floor, even when they’re not totally reaching customers but. Core PCE, the Fed’s most popular gauge, is anticipated to tick up modestly to a 2.6 p.c year-over-year tempo, supported by particular classes however restrained by disinflation in healthcare and journey. The Federal Reserve is more likely to stay cautious, seeing early indicators of tariff-related value pressures however recognizing that consumer-side weak point continues to dampen broader inflation momentum. In sum, inflation stays subdued for now, however indicators of underlying firm-level value pressure and uneven pass-through counsel the disinflationary pattern might show fragile within the months forward.

US manufacturing and providers sectors each confirmed indicators of stress in Could, reinforcing the image of a fragile, uneven enlargement described within the newest inflation knowledge. The ISM Manufacturing Index slipped additional into contraction at 48.5, as corporations reported softening demand, tariff-related uncertainty, and vital declines in each imports and exports — with the previous plunging to a 16-year low. Stock drawdowns and lengthening provider supply occasions counsel disarray in provide chains, whereas order backlogs continued to shrink. Trade feedback mirrored frustration over chaotic commerce coverage and its impression on pricing, profitability, and funding plans. In the meantime, the ISM Providers Index fell to 49.9 — its first contraction since 2022 — pushed by a steep drop in new orders and delayed buying choices amid federal funds cuts and tariff coverage confusion. Though costs paid by service suppliers jumped to their highest since 2022, respondents famous that a lot of the burden was being absorbed through revenue margins quite than handed on to customers. Taken collectively, the information present that at the same time as headline inflation stays muted, enterprise sentiment and forward-looking demand indicators throughout each manufacturing and providers are deteriorating below the burden of persistent coverage uncertainty and price pressures — elevating the chance that company pressure, quite than client weak point, will be the subsequent stage of this financial slowdown.

Labor market circumstances in Could counsel a slow-burn deterioration beneath a still-stable floor. Headline nonfarm payrolls rose by 139,000 — modestly above expectations — however downward revisions to earlier months and a flat unemployment charge of 4.2 p.c conceal deeper fragilities. ADP’s personal payroll knowledge confirmed solely 37,000 jobs added, the weakest in two years, with enterprise providers, training, and manufacturing shedding staff. Sectors most uncovered to tariffs — like transportation and manufacturing — continued to underperform, whereas job losses in momentary assist and federal employment sign rising warning. Hiring is clearly slowing, however employers aren’t but participating in mass layoffs — what some economists describe as a “low-hiring, low-firing” equilibrium. The labor pressure shrank by over 600,000 in Could, and long-term unemployment as a share of complete joblessness stays elevated at over 20 p.c, regardless of a superficial decline. In the meantime, wage progress — at 3.9 p.c year-over-year — stays resilient, reflecting corporations’ reluctance to shed staff regardless of value and demand uncertainty.

A deeper look into the labor dynamics reveals a cooling jobs market marked by rising mismatches and rising structural challenges. The job-finding charge continues to fall, as does the quits charge, suggesting that staff are each much less capable of finding new jobs and fewer prepared to danger leaving present positions. The U-6 broader unemployment charge, which incorporates discouraged and underemployed staff, held regular at 7.8 p.c, reinforcing that headline numbers understate slack. Skilled and enterprise providers employment — a proxy for white-collar sectors — stays stagnant, whereas job creation is concentrated in well being care and development, intensifying a bifurcation in labor alternatives. Many jobseekers, particularly in high-skill sectors, face extended job hunts or underemployment. Regardless of President Trump’s tariff pause on some items and continued strain on Fed Chair Powell to chop charges, hiring hesitance pushed by tariff unpredictability, shrinking public sector employment, and sectoral divergences suggests a labor market shedding traction. Total, whereas the floor knowledge helps a story of resilience, the underlying indicators reveal mounting pressure — with the economic system precariously balancing between stagnation and slippage.

Client and enterprise sentiment each confirmed significant enhancements in latest weeks, however the rebound stays fragile and closely contingent on coverage readability. The College of Michigan’s client sentiment index jumped 8.3 factors in June — the most important acquire in 17 months — as inflation expectations eased sharply, particularly for the one-year horizon, which fell from 6.6 p.c to five.1 p.c. Shoppers additionally reported the strongest enchancment in private finance expectations in over three years, suggesting a tentative stabilization after weeks of volatility tied to President Trump’s sweeping tariff hikes. Nevertheless, views on general enterprise circumstances and shopping for climates stay subdued relative to late 2024, reflecting lingering nervousness. In the meantime, the NFIB’s Small Enterprise Optimism Index rose 3.0 factors to 98.8 in Could, led by improved expectations for gross sales and enterprise circumstances. Capital spending plans and anticipated value hikes each elevated, signaling confidence in demand, but an elevated uncertainty index and falling earnings developments level to unresolved issues about enter prices and federal coverage unpredictability — together with the delayed tax and spending invoice touted as a lift for small enterprises.

Collectively, the sentiment readings illustrate a US economic system at a psychological inflection level: a inhabitants cautiously hopeful in regards to the future, but clearly reactive to unpredictable federal actions. Each households and small corporations are responding positively to a pause in tariff escalation and indicators of fiscal help on the horizon, however they continue to be weak to any renewed coverage shocks. Importantly, the improved client outlook could assist maintain spending within the close to time period, at the same time as enterprise hiring and funding keep subdued. Nonetheless, elevated uncertainty metrics in each surveys counsel that optimism is conditional quite than sturdy. For financial progress to reaccelerate meaningfully, greater than momentary aid is required — readability on commerce, inflation containment, and a reputable fiscal path could be essential to convert tentative optimism into sustained enlargement.

Retail gross sales declined for a second consecutive month in Could, dropping 0.9 p.c — the steepest fall since early 2025 — as customers reacted to tariff-driven value uncertainty and tighter family funds. The pullback was concentrated in autos, constructing supplies, and gasoline, suggesting an finish to front-loaded purchases made forward of anticipated tariff hikes. Broader indicators of demand, together with a drop in industrial manufacturing and the bottom homebuilder sentiment since 2022, bolstered indicators of client warning. Nevertheless, control-group gross sales — which feed into GDP calculations — rose 0.4 p.c, providing a silver lining and suggesting underlying consumption stays resilient. Whereas massive retailers notice that customers are nonetheless coming in, they’re changing into extra selective, specializing in necessities and scaling again discretionary purchases. The information mirror a bifurcation: higher-income customers are holding up nicely, whereas middle- and lower-income households are adjusting habits amid ongoing financial nervousness. The blended report highlights a fragile consumption panorama that, whereas not collapsing, is more and more formed by volatility in costs, coverage, and sentiment.

Additional again within the time period construction from client items, US manufacturing and industrial output knowledge reveal a murky image of a sector straining below uneven coverage indicators and rising enter prices. Manufacturing unit manufacturing declined 0.4 p.c in April and industrial manufacturing dipped one other 0.2 p.c in Could, weighed down by weaker output in client items, nondurables, and utilities. Whereas auto and aerospace manufacturing offered remoted energy — probably a front-loaded response to tariff threats — broader industrial exercise stays subdued, with capability utilization falling to 77.4 p.c. Manufacturing of enterprise gear eked out beneficial properties, however nondurable items output declined regardless of an uptick in mixture hours labored, suggesting productiveness shortfalls. The three-month decline in client items output displays not simply softening demand however lingering uncertainty that has stalled capital expenditure plans and dragged on manufacturing facility sentiment indices. Surveys just like the ISM stay in contraction territory, reinforcing anecdotal proof that corporations are delaying hiring and funding choices till tariff paths and financial measures change into clearer. The sector’s volatility and conflicting indicators illustrate a fragile manufacturing base extra reactive than resilient — one that might battle to get better momentum with out decisive and coherent commerce and tax coverage from Washington.

The Federal Reserve continues to tread cautiously, holding rates of interest regular for a fourth consecutive assembly whereas signaling each a softer labor market and protracted inflation dangers. Though the median forecast nonetheless implies 50 foundation factors of charge cuts in 2025, the distribution of views inside the FOMC has widened significantly, with almost equal weight behind both no cuts or two. Revised financial projections mirror a slower return to the impartial charge, with core PCE inflation expectations rising modestly via 2027 and unemployment estimates nudging greater. Chair Jerome Powell struck a extra hawkish tone throughout his press convention, emphasizing tariff-related inflation pressures and the resilience of employment knowledge. Regardless of this, market members interpreted the median charge path as modestly dovish, pricing in a slight improve in anticipated easing. The general image is one among rising uncertainty, with inner divisions on the FOMC mirroring broader volatility within the financial knowledge. The Fed stays on maintain, awaiting larger readability on the cumulative results of tariffs, client value pass-through, and labor market dynamics.

In the meantime, fiscal coverage is more and more outlined by partisan urgency and legislative congestion, with three concurrent budgetary battles underway. The centerpiece is the GOP’s reconciliation package deal—a sweeping tax minimize extension and spending invoice with a ten-year, $2.4 trillion debt impression, dealing with inner Republican friction over Medicaid cuts and inexperienced subsidies. Extra efforts embody a extra modest rescission plan focusing on $9.4 billion in discretionary cuts, and the annual appropriations course of, which dangers a authorities shutdown if no settlement is reached by September 30. Democrats are largely sidelined from reconciliation, however are making ready to leverage the invoice’s political liabilities—corresponding to expanded uninsured ranks and large deficits—heading into 2026. Including complexity is the administration’s assumption that prime tariff revenues will offset misplaced tax earnings, a state of affairs depending on unsure long-term commerce coverage. In tandem, the financial and financial landscapes reveal a fractured coverage setting: financial easing stays tentative, whereas fiscal enlargement barrels ahead with restricted bipartisan consensus. The mixed impact could show pro-cyclical on the flawed second—stimulative fiscal coverage colliding with a Fed reluctant to declare victory over inflation.

The current financial outlook is being expressed via comfortable floor knowledge sitting atop solidifying structural strains. Inflation readings stay subdued on the patron facet, but firm-level knowledge present rising producer costs and margin compression, hinting at suppressed value pressures with an unclear timing of impending tariff pass-throughs. Manufacturing and providers exercise proceed to contract, with provide chain dysfunction and commerce coverage uncertainty weighing on funding and hiring. Labor market indicators current a secure façade, however reveal a deeper deterioration in participation, job-finding, and sectoral stability — notably in tariff-sensitive industries. Client and enterprise sentiment have improved modestly, however stay fragile, extremely depending on coverage stability, and uneven throughout earnings ranges. Fiscal coverage, in the meantime, is charging forward with expansive tax cuts and spending proposals, whereas financial coverage stays cautious, its easing path clouded by inner FOMC divisions and ongoing inflationary danger. Collectively, this produces a coverage collision course the place stimulative fiscal actions could amplify the very inflationary dynamics the Fed seeks to restrain.

In sum, the US economic system is balancing on a narrowing ledge: demand stays intact however more and more selective, sentiment is conditionally optimistic, and hiring continues at a slowing tempo in an more and more bifurcated labor market. With core PCE more likely to tick greater and industrial knowledge exhibiting indicators of stagnation, the actual economic system is absorbing extra stress than headline indicators counsel. A clearer outlook depends upon solutions to a number of urgent questions: Will tariff-related value pressures cross via extra forcefully to customers this fall? Can fiscal stimulus offset deteriorating enterprise funding with out overheating demand? And the way credible is the present path of coverage restraint if labor market slack re-emerges?

Till these uncertainties resolve, the US economic system stays singularly weak to uneven shocks: a system stabilizing for now, however depending on coherence between Washington’s fiscal ambitions and the Fed’s inflation-fighting resolve.

LEADING INDICATORS

ROUGHLY COINCIDENT INDICATORS

LAGGING INDICATORS

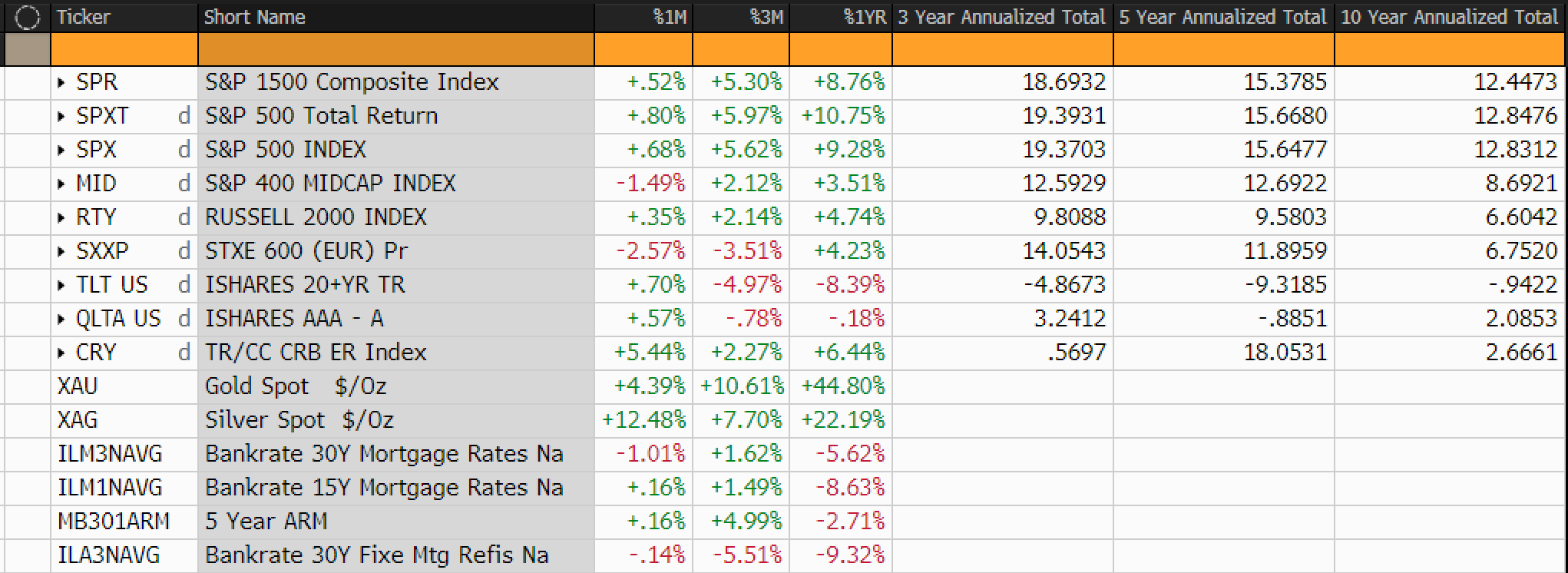

CAPITAL MARKET PERFORMANCE